Many homeowners in Greeneville, TN, assume that once an insurance claim is approved, the insurance company will automatically pay the full amount needed for roof replacement. Before filing a claim, it helps to understand how to check for roof damage after a storm so you can document everything accurately. In reality, many claims are partially approved, underpaid, or delayed because important details were missed during inspection or documentation. Insurance companies often rely on adjuster reports, policy wording, and visible evidence to determine payment amounts, which means homeowners who are not prepared can end up paying high out-of-pocket costs even after filing a claim.

Roof replacement negotiation is not about arguing aggressively with insurance companies. It is about understanding your policy, documenting roof damage properly, and making sure the insurance estimate reflects the actual condition of the roof. Storm damage, wind uplift, hail impact, and hidden moisture problems are not always fully visible during a quick inspection, which is why preparation and professional support matter. For homeowners dealing with storm-related roof damage in Tennessee, knowing how the process works can make a major difference in the final settlement amount.

When Insurance Will Pay for Roof Replacement

Insurance companies generally pay for roof replacement when damage is caused by sudden events that are covered under the homeowner’s policy. Common covered events include windstorms, hail damage, falling trees, fire damage, and severe weather conditions. If a storm creates enough damage to affect the roof’s ability to protect the home, insurance may approve either partial repairs or full replacement, depending on the severity of the damage.

However, insurance policies usually do not cover roofs damaged by old age, neglect, poor maintenance, or gradual wear and tear. This is one of the biggest reasons claims get denied. If shingles were already failing before the storm occurred, the insurance company may argue that the damage was caused by age rather than the weather event itself.

Another important factor is the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV) policies. RCV policies generally cover the cost to replace the roof using similar materials, while ACV policies reduce payment based on depreciation and roof age. Older roofs often receive smaller payouts under ACV coverage because the insurance company subtracts years of wear from the claim amount.

Understand Your Homeowners Insurance Policy Before Negotiating

Before discussing roof replacement with an insurance adjuster, homeowners should understand what their policy actually covers. Many people file claims without reviewing deductibles, exclusions, or payment limitations, which creates confusion during negotiations later in the process. A deductible is the amount the homeowner must pay before insurance coverage applies. Some policies also include separate wind or hail deductibles, which can be higher than standard deductibles. Understanding these details helps homeowners estimate actual out-of-pocket costs before negotiations begin.

Policies may also contain roof age restrictions. Some insurance companies reduce coverage once the roof reaches a certain age, especially for older asphalt shingle systems. In these situations, the claim may only qualify for partial reimbursement rather than full replacement cost coverage. Local building codes also matter during negotiations. If Tennessee building codes require additional materials or upgrades during replacement, these costs may sometimes be included through supplements or code compliance adjustments. Homeowners who understand these policy details are usually in a stronger position during claim discussions because they can identify missing items or incorrect assumptions in the insurance estimate.

Start With a Professional Roof Inspection

One of the most important steps in roof insurance negotiation is getting a professional roof inspection before filing the claim. Many forms of storm damage are difficult for homeowners to identify from the ground, especially after hailstorms or strong wind events. Missing shingles may be obvious, but hidden issues such as lifted shingles, cracked seal strips, bruised asphalt, or flashing damage often require a trained inspection.

A professional roofing contractor documents roof conditions using photographs, measurements, inspection notes, and sometimes drone imaging. This documentation creates evidence that can support the insurance claim and helps reduce the risk of important damage being overlooked during the adjuster inspection.

Professional inspections are especially important in Greeneville, TN, because severe weather can create damage that is not immediately visible inside the home. Small roof failures may continue worsening long after the storm passes, eventually leading to leaks, moisture damage, or mold growth.

Document Everything Before Filing the Claim

Strong documentation is one of the biggest factors that improve roof insurance negotiations. Following a systematic process to document storm damage for insurance claims ensures all visible and hidden issues are supported with evidence. Insurance companies rely heavily on evidence when reviewing claims, so homeowners should gather as much information as possible before the adjuster visits.

Useful documentation includes:

- Photos of damaged shingles

- Videos showing visible roof issues

- Interior leak stains or ceiling damage

- Fallen tree limbs or storm debris

- Previous maintenance and repair records

- Dates of major storms in the area

Photographs should be clear and taken from multiple angles whenever possible. Interior damage should also be documented because leaks inside the home often help prove that roof damage affected the structure. Keeping organized records makes communication with the insurance company easier and reduces confusion during negotiations. Homeowners who provide complete documentation are often in a stronger position when requesting reconsideration or supplements later in the process.

File the Roof Insurance Claim Quickly

Timing matters after storm damage occurs. Most insurance policies require claims to be reported within a specific time period after the event. Waiting too long can make it harder to prove that the damage was caused by the covered storm rather than normal aging.

Homeowners should contact their insurance company as soon as possible after discovering roof damage. During the filing process, the insurance company usually asks for:

- Date of loss

- Description of the damage

- Photos or inspection reports

- Emergency repair information

Temporary repairs may also be necessary to prevent additional interior damage while waiting for claim approval. For example, tarping exposed roof sections can help reduce water intrusion after severe storms. However, homeowners should avoid making major permanent repairs before the insurance inspection occurs because this can make it harder for adjusters to evaluate original storm damage accurately.

Professional roof inspections and claim support help homeowners understand what damage exists before negotiations begin. For homeowners in Greeneville, TN, working with experienced roofing professionals from Covenant Roofing & Restoration can help identify hidden storm damage, improve documentation quality, and support fair roof replacement evaluations during the insurance process.

How Insurance Adjusters Evaluate Roof Claims

After a roof insurance claim is filed, the insurance company schedules an inspection with an adjuster to evaluate the damage. The adjuster’s job is to determine whether the roof damage qualifies under the homeowner’s policy and estimate how much the insurance company should pay for repairs or replacement. This inspection is one of the most important stages in the entire negotiation process because the adjuster’s report heavily influences the settlement amount.

During the inspection, adjusters typically look for signs of storm-related damage such as lifted shingles, hail bruising, broken seal strips, missing roofing materials, flashing damage, and water intrusion points. They also evaluate the roof’s age and overall condition to determine whether the damage was caused by a covered event or by gradual deterioration.

One common issue homeowners face is that some forms of storm damage are difficult to identify during a short inspection. Small hail impacts, weakened shingle seals, or hidden moisture damage may be overlooked, especially if the adjuster spends limited time on the roof. This is why many homeowners choose to have a roofing contractor present during the inspection. A contractor can point out damage areas, explain roofing system issues, and help ensure the inspection reflects the actual roof condition.

How to Negotiate Roof Replacement With Insurance

Negotiating a roof replacement with insurance is less about pressure and more about structure, proof, and clear communication. Insurance companies operate on documentation, policy language, and adjuster reports, so homeowners who stay organized usually get better outcomes than those who rely solely on verbal discussions. In Greeneville, TN, where storm-damage roof insurance claims are common, understanding how to respond properly at each stage of the negotiation process can directly affect how much of the roof replacement cost is covered.

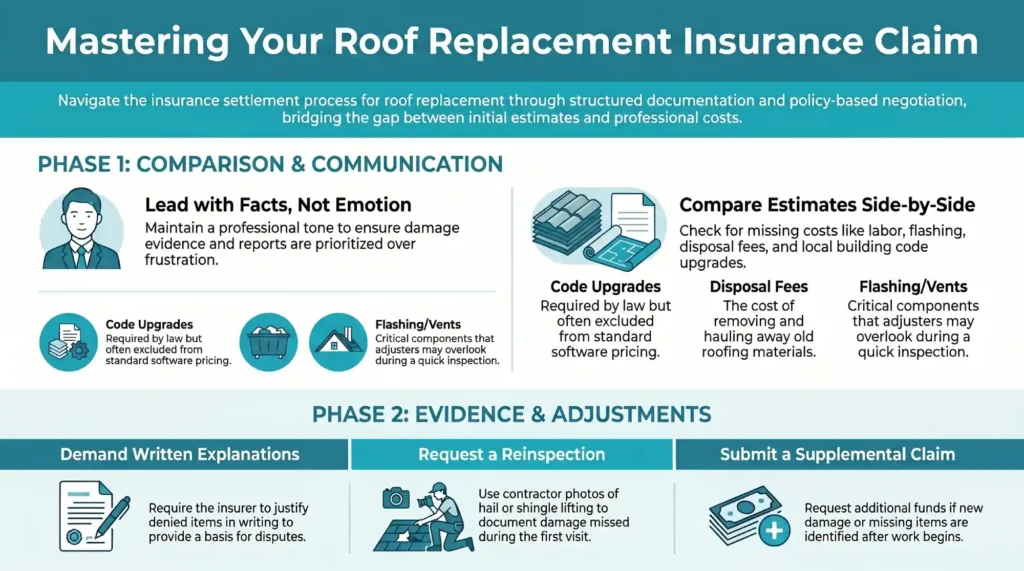

Stay Calm and Professional During Communication

One of the most important parts of insurance negotiation is maintaining a calm and professional tone in every interaction. Insurance claims often involve delays, revisions, and multiple reviews, which can frustrate homeowners. However, emotional or aggressive communication rarely improves results and may slow the process further.

A clear, respectful approach helps build better cooperation between the homeowner and insurance adjuster. It also ensures that important details are properly recorded and reviewed. Keeping conversations factual, focused on roof damage evidence, inspection reports, and policy coverage, creates a stronger position during negotiation.

Compare the Insurance Estimate With the Contractor Estimate

Insurance companies often produce estimates based on standardized pricing systems, but these estimates do not always match real contractor pricing in the local market. Because of this, comparing the insurance scope of work with a detailed contractor estimate is one of the most important steps in negotiation.

A contractor estimate may include items such as:

- Full roof replacement materials

- Labor costs based on local rates

- Underlayment and flashing replacement

- Disposal fees and cleanup

- Code-required upgrades

If the insurance estimate is missing any of these components, the total payout may fall short of actual replacement costs. Identifying these differences early allows homeowners to request corrections or additional payments through supplements.

Ask for Written Explanations for Denied Items

When an insurance company reduces or denies parts of a roof claim, homeowners should always request written explanations. Verbal responses are not enough because they cannot be reviewed later or used for formal disputes.

Written explanations help clarify:

- Why were specific roofing items excluded

- Whether the damage was classified as wear and tear

- If policy limitations affected coverage

- Whether documentation was considered insufficient

This step is important because it forces the insurance company to clearly justify their decision. In many cases, missing or denied items can be reconsidered if additional evidence is provided, such as contractor reports, inspection photos, or updated storm documentation. If only minor areas are affected, roof repair services in Greeneville can address problems before full replacement is required.

Request Reinspection if Damage Was Missed

Roof inspections are often limited in time, and some forms of storm damage are not visible during a single visit. If important issues were missed during the first inspection, homeowners have the right to request a reinspection.

Reinspection is especially useful when:

- Hail damage was overlooked

- Shingle lifting was not fully documented

- Hidden leaks or flashing issues were missed

- Contractor findings differ from adjuster findings

During reinspection, providing additional documentation from a roofing contractor can help support the request. This may include updated photos, detailed reports, or measurements that show damage was more extensive than originally recorded.

Understanding Scope of Loss and Repair Pricing

The “scope of loss” is the official insurance document that outlines what the company agrees to pay for roof repairs or replacement. This document includes material quantities, labor costs, and approved repair items. However, it is not always complete.

Many homeowners assume the scope of loss includes everything needed for a full roof replacement, but important items are sometimes missing, such as:

- Flashing replacement

- Drip edge installation

- Ventilation improvements

- Ice and water shield coverage

- Disposal and cleanup costs

- Local building code upgrades

Repair pricing within the scope is often based on software pricing systems, which may not fully reflect current material or labor rates in Greeneville, TN. Because of this, reviewing the scope carefully with a roofing contractor helps identify missing costs before work begins.

How to Challenge Low Settlement Offers Properly

Low settlement offers are common in roof insurance claims, especially when initial inspections miss damage or when estimates do not include full replacement costs. Challenging a low offer should always be done using documentation rather than opinion.

A proper challenge includes:

- Contractor estimates showing real replacement costs

- Photos and videos of storm damage

- Inspection reports identifying hidden issues

- Comparison of insurance scope vs actual roof needs

Homeowners can also request a supplemental claim if new damage or missing items are identified after the initial estimate. In some cases, a second inspection or independent review can help correct underpaid claims.

Roof Claim Supplements Explained

Supplements are additional requests submitted to the insurance company when extra work or hidden damage is discovered after the original estimate was created. Supplements are very common in roofing claims because some problems are impossible to identify fully until shingles are removed during construction.

For example, contractors may discover:

- Rotten roof decking

- Hidden moisture damage

- Ventilation deficiencies

- Additional flashing damage

- Code-required upgrades not included initially

When this happens, the contractor submits supporting documentation, photos, and updated pricing to the insurance company for review. If approved, the insurance company issues additional payment to cover the newly identified work.

Supplements are not fraudulent or unusual; they are a normal part of many roof replacement projects because roofing systems often contain hidden layers that cannot be inspected visually during the first adjuster visit.

Common Reasons Roof Claims Get Denied

Roof insurance claims are denied for several reasons, and many denials happen because homeowners misunderstand what their policy actually covers. One of the most common denial reasons is normal wear and tear. Insurance companies generally cover sudden accidental damage, not gradual aging or neglected maintenance.

Claims may also be denied if:

- The roof was already near failure before the storm

- Damage cannot be connected clearly to the reported event

- The homeowner waited too long to file the claim

- Documentation is incomplete or inconsistent

- Maintenance history is missing

Older roofs face additional challenges because insurance companies may argue that existing deterioration contributed to the damage. This is why early inspections and detailed documentation are so important after storms occur.

Another issue involves improper repairs made before the inspection. If temporary repairs alter the visible damage too heavily, adjusters may struggle to determine the original storm impact, which can complicate claim approval.

What to Do If Your Roof Claim Is Denied or Underpaid

A denied or underpaid roof claim does not always mean the process is over. Homeowners still have several options if they believe the insurance company overlooked important damage or underestimated repair costs. The first step is requesting a detailed explanation of the denial or reduced payment. This helps identify whether additional documentation, contractor estimates, or inspection reports may strengthen the claim. In some cases, requesting a second inspection can lead to revised findings, especially if storm damage was missed during the initial visit.

Homeowners may also work with:

- Independent adjusters

- Public adjusters

- Roofing contractors experienced in insurance claims

These professionals review documentation and help identify differences between actual roof conditions and the insurance company’s estimate. If disagreements remain unresolved, homeowners may need legal guidance, especially in cases involving major underpayment or policy interpretation disputes. However, many claim disagreements are resolved through additional inspections and supplemental documentation before legal action becomes necessary.

For homeowners in Greeneville, TN, storm-related roof damage inspections from Covenant Roofing & Restoration help identify hidden roofing issues before negotiations move forward. Contractor-supported inspections and estimate reviews often help homeowners understand whether their claim reflects the actual condition of the roof.

Common Mistakes Homeowners Make During Roof Negotiations

Many homeowners weaken their own insurance claims without realizing it. Small mistakes during the claim process can reduce settlement amounts, delay approvals, or even lead to claim denial. One of the most common mistakes is accepting the first insurance offer without reviewing the estimate carefully. Initial estimates sometimes miss roofing components, labor costs, or code-required upgrades, which can leave homeowners paying unexpected expenses later.

Another major mistake is waiting too long after a storm to report damage. Delayed claims make it harder to prove that the damage came from the reported weather event instead of normal aging or poor maintenance. Insurance companies may use delays as part of their reasoning for denial or reduced payouts.

Some homeowners also sign roofing contracts before understanding their insurance settlement details. This can create confusion if the insurance company approves less coverage than expected. Choosing inexperienced or unlicensed contractors is another serious issue because poor workmanship and inaccurate estimates can complicate negotiations further.

Failing to document conversations with adjusters, contractors, and insurance representatives can also create problems later in the process. Keeping records of emails, estimates, inspection reports, and claim numbers helps homeowners stay organized and reduces misunderstandings during negotiations.

How Roofing Contractors Help With Insurance Claims

Experienced roofing contractors often play a major role during roof insurance claim negotiation because they understand both roofing systems and claim procedures. Contractors help homeowners identify storm damage, prepare documentation, and compare insurance estimates with actual replacement needs.

One important benefit of working with an experienced roofing company is having contractor support during the adjuster inspection. Contractors can explain roofing damage directly on-site and point out areas that may otherwise be missed during a brief inspection. This is especially useful for identifying hail impacts, lifted shingles, flashing problems, or ventilation-related damage.

Roofing contractors also help review the insurance scope of loss and identify missing items such as:

- Underlayment replacement

- Flashing upgrades

- Drip edge installation

- Code-required ventilation improvements

- Disposal and labor costs

If additional damage is discovered during construction, contractors may submit supplements with supporting photos and documentation to request additional insurance payment. This process helps ensure the roof replacement reflects actual repair needs rather than incomplete estimates.

For homeowners in Greeneville, TN, experienced local contractors are also familiar with regional weather conditions and Tennessee roofing requirements, which can improve claim accuracy and reduce construction delays.

Roof Replacement Insurance Process Timeline

Understanding the roof insurance timeline helps homeowners know what to expect during negotiations and replacement. While every claim is different, most roof replacement claims follow a similar process from inspection to final payment.

| Stage | What Happens |

| Initial Roof Inspection | Contractor or homeowner identifies storm damage |

| Claim Filing | Insurance company receives claim information |

| Adjuster Inspection | Insurance adjuster evaluates roof condition |

| Estimate Review | Insurance company creates settlement estimate |

| Negotiation & Supplements | Missing items or hidden damage are addressed |

| Claim Approval | Insurance issues payment based on coverage |

| Roof Replacement | Contractor completes roofing work |

| Final Payment Release | Remaining depreciation or supplement funds are paid |

The timeline varies depending on weather events, insurance response speed, documentation quality, and contractor scheduling. Large regional storms often create claim backlogs, which may slow inspections and approvals.

Tips for Homeowners in Greeneville, TN

Homes in Greeneville, TN experience seasonal storms, heavy rain, humidity, and occasional wind damage that can affect roofing systems over time. Because weather conditions in Tennessee change throughout the year, roof damage is not always immediately visible after storms pass.

Homeowners should schedule inspections after:

- Strong wind events

- Hailstorms

- Heavy rainfall

- Falling tree limb impact

- Sudden interior leaks

Fast inspections help document storm-related damage before evidence begins fading due to weather exposure or temporary repairs. Tennessee building code requirements may also affect roofing claims if upgrades are necessary during replacement. This is another reason local roofing experience matters during roof insurance claim negotiation. Working with contractors familiar with Greeneville weather patterns and roofing requirements helps homeowners identify realistic replacement needs and avoid missing important claim details.

Frequently Asked Questions

What should I avoid saying to a roof insurance adjuster?

Homeowners should avoid guessing about damage causes or minimizing visible problems. It is better to stick to factual observations and provide documentation rather than assumptions.

Can insurance deny an old roof claim?

Yes. Insurance companies often deny claims if they believe the roof damage resulted mainly from age, wear and tear, or poor maintenance rather than sudden storm-related damage.

What are roofing supplements?

Supplements are additional requests submitted to insurance companies when hidden damage or extra work is discovered after the original estimate was created.

Should my roofing contractor meet the insurance adjuster?

In many cases, yes. Contractor presence during inspections helps identify overlooked roofing damage and improves communication about replacement requirements.

What if the insurance estimate is too low?

Homeowners can request a reinspection, submit contractor estimates, provide additional documentation, or ask for supplements if important roofing items were missed.

How long does a roof insurance claim take?

Simple claims may move quickly, while larger storm claims or disputed settlements may take several weeks or longer, depending on inspections, supplements, and insurance processing times.

Final Conclusion: Getting Fair Roof Replacement Coverage

Negotiating roof replacement with insurance companies requires preparation, documentation, and patience. Many homeowners assume the insurance company automatically includes every necessary repair cost, but real roofing claims often involve estimate reviews, supplemental requests, and detailed inspections before fair coverage is reached. Understanding your policy, documenting damage carefully, and working with experienced roofing professionals can significantly improve the chances of receiving proper roof replacement coverage.

In areas like Greeneville, TN, where storms and seasonal weather frequently affect roofing systems, fast inspections and organized claim preparation are especially important. Professional roofing support also helps homeowners understand whether the insurance estimate truly reflects the roof’s actual condition. Local guidance from Covenant Roofing & Restoration helps homeowners identify storm damage, review insurance estimates, and move through the roof replacement process with clearer expectations and stronger documentation.