A metal roof can be one of the strongest upgrades you make to your home, but the upfront price can make many homeowners pause. For families in Greeneville, TN, this decision often comes at the worst time: an aging roof starts leaking, storm damage exposes weak spots, or rising repair costs make replacement hard to delay. Financing a metal roof can help turn one large project cost into planned monthly payments, giving you a way to protect your home without draining savings all at once. The key is understanding your loan options, how monthly payments work, what lenders look for, and why a clear roof estimate from Covenant Roofing & Restoration should come before choosing any financing plan.

Quick Answer: Can You Finance a Metal Roof?

Yes, you can finance a metal roof through contractor financing, dealer financing, a personal loan, home equity loan, HELOC, credit card, renovation loan, or cash-out refinance. The best option depends on your roof cost, credit score, available home equity, interest rate, loan term, monthly budget, and how quickly the roof needs to be replaced. Many homeowners choose financing because metal roofing costs more upfront than asphalt shingles, but it can provide strong long-term value when installed correctly.

Before applying, it is smart to get a professional roof inspection and written estimate. That estimate helps you understand whether you need a full metal roof replacement, roof repair, storm damage repair, or a different roofing solution. Covenant Roofing & Restoration can help Greeneville homeowners review roof condition, compare material choices, and understand project scope before they make a financing decision.

Why Financing a Metal Roof Makes Sense

Financing a metal roof makes sense when the roof needs attention but paying the full amount upfront would put pressure on household savings. A roof protects everything inside the home, so delaying replacement because of cost can lead to leaks, water damage, insulation problems, damaged drywall, and more expensive repairs later. Financing gives homeowners a way to act sooner while spreading the cost into monthly roof payments.

For many Greeneville homeowners, metal roofing is also a long-term upgrade. Standing seam metal roofs, metal shingles, and higher-grade metal panels can cost more than basic roofing systems, but they may offer better durability, curb appeal, and storm resistance. Financing can make it easier to choose a better roof system instead of settling for the cheapest short-term option.

Manage High Upfront Costs

Metal roofing projects can include more than panels alone. The total cost may include tear-off, decking repairs, underlayment, flashing, trim, ridge caps, ventilation updates, labor, and cleanup. If the roof has storm damage, old shingles, soft decking, or poor ventilation, the final project cost can rise beyond the price of the metal panels.

Financing helps convert that total project cost into fixed monthly payments. Instead of delaying the work or using all available savings, homeowners can choose a payment plan that fits their budget. This can be especially helpful when the roof is already leaking, showing signs of age, or failing after severe weather.

Upgrade Materials and Protect Home Value

Financing can also help homeowners choose stronger materials. A metal roof project may include standing seam panels, metal shingles, better metal gauge, higher-quality underlayment, improved flashing, and stronger warranty coverage. These upgrades may cost more at the start, but they can support better long-term roof performance.

For homeowners planning to stay in their home, a better roof can reduce repair stress and improve curb appeal. For homeowners thinking about selling later, a properly installed metal roof can also make the property more attractive to buyers. The goal is not just to finance any roof. The goal is to finance the right roof system for the home.

Pay for Storm Repairs or Insurance Deductibles

Financing may also help after storm damage. If wind, hail, or heavy rain damages the roof, homeowners may need fast repair or replacement before the next storm. Even when insurance is involved, there may still be a deductible, uncovered upgrades, or costs that need to be paid before work begins. A financing option can help cover those out-of-pocket costs. Covenant Roofing & Restoration can inspect storm damage, provide documentation, and explain repair or replacement options so homeowners understand what needs to be financed and what may be handled through insurance.

Main Metal Roof Financing Options

There is no single best financing option for every homeowner. Some people need fast approval. Some want the lowest possible interest rate. Some have home equity. Others prefer an unsecured personal loan because they do not want to use the home as collateral. The right choice depends on your financial situation, project urgency, and comfort with different types of debt. Before choosing, compare the APR, loan term, monthly payment, fees, prepayment rules, deferred interest terms, and total cost over the life of the loan. A low monthly payment can look attractive, but it may cost more over time if the loan term is long or the interest rate is high.

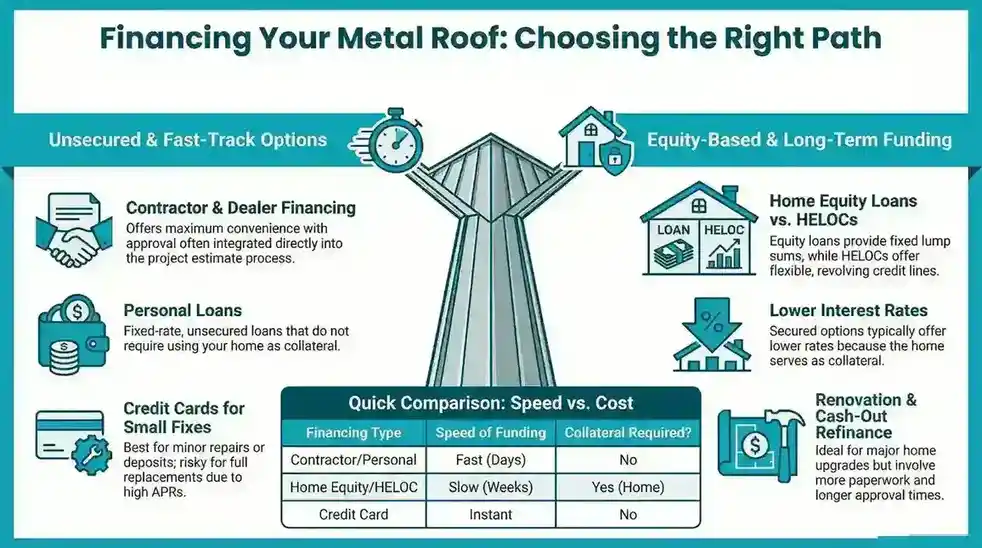

Contractor or Dealer Financing

Contractor financing, sometimes called dealer financing, is offered through roofing companies and third-party lending partners. Some roofing contractors work with financing platforms such as Hearth or GreenSky, while others may offer lender-backed programs through manufacturer or dealer networks. These plans may include fixed monthly payments, 0% down options, same-as-cash promotions, deferred interest, or short-term no-interest offers depending on approval and lender terms. The main benefit is convenience. Homeowners can review the roof estimate and financing options in the same project process. This can help when the roof needs replacement quickly and the homeowner does not want to spend weeks comparing banks. The main caution is that every financing offer should be read carefully. Same-as-cash and deferred interest plans can become costly if the balance is not paid within the promotional period.

Personal Loans

A personal loan is an unsecured loan that can be used for roof replacement, roof repair, or a metal roofing upgrade. Since it does not require home equity, it may be useful for homeowners who do not want to borrow against their house. Personal loans often have fixed interest rates, fixed repayment terms, and predictable monthly payments. Approval usually depends on credit score, income, employment, debt-to-income ratio, and lender requirements. Many lenders may prefer borrowers with fair to strong credit, and stronger credit scores often qualify for better rates. A personal loan can also fund faster than home equity options, which may help if the roof needs urgent replacement.

Home Equity Loan

A home equity loan lets homeowners borrow a lump sum using home equity as collateral. This option may offer lower interest rates than unsecured personal loans because the loan is secured by the home. It can work well for larger metal roof projects where the homeowner wants a set loan amount and a fixed repayment schedule. The main risk is that the home is used as collateral. If payments are missed, the lender has a claim against the property. Home equity loans may also involve closing costs, appraisals, and a longer approval process. This option may be better for homeowners with strong equity who are comfortable with a secured loan.

HELOC

A HELOC, or home equity line of credit, is also based on home equity, but it works more like a revolving credit line. Instead of receiving one lump sum, homeowners can borrow as needed up to a set limit. This can be useful if the roof project is part of a larger home improvement plan, such as gutters, siding, ventilation, or interior repairs after water damage. The main benefit is flexibility. The main risk is that many HELOCs have variable interest rates, which means the monthly payment can change. Like a home equity loan, the home is collateral. Greeneville homeowners should compare HELOC terms carefully before using this option for metal roof financing.

Credit Cards

Credit cards are usually best for small roof repairs, deposits, or short-term balances that can be paid quickly. Some cards offer 0% introductory APR periods, which may be helpful if the balance can be paid before the promotional period ends. For a full metal roof replacement, credit cards are often risky because standard APRs can be high. If the balance remains after the 0% period, interest charges can increase the total cost quickly. Credit cards should be used with a clear payoff plan, especially for large roofing projects.

Renovation Loans or Cash-Out Refinance

Renovation loans and cash-out refinancing may work for larger home improvement plans. A renovation loan is often tied to property improvements, while a cash-out refinance replaces the existing mortgage with a larger loan and gives the homeowner cash from the difference. These options may provide access to larger amounts, but they usually involve more paperwork, closing costs, and longer approval times. This type of financing may make sense if the metal roof is part of a broader home upgrade. It may not be the fastest option if the roof needs urgent attention after a storm or active leak.

Metal Roof Financing Options Compared

Choosing a financing option should not be based on one factor alone. A homeowner should compare speed, monthly payment, risk, interest rate, collateral, and total repayment cost. A fast loan may have a higher rate. A lower-rate loan may require home equity and more time. A promotional plan may look affordable, but it may have strict payoff rules.

| Financing Option | Best For | Main Benefit | Main Risk |

| Contractor financing | Fast roof replacement | Convenient and project-focused | Terms vary by lender |

| Personal loan | No home equity needed | Fixed payments and fast funding | Higher APR than secured loans |

| Home equity loan | Larger projects | Lower possible rate | Home used as collateral |

| HELOC | Flexible borrowing | Borrow as needed | Variable rates and collateral risk |

| Credit card | Small repair or 0% promo payoff | Quick access | High APR if not paid fast |

| Cash-out refinance | Large home upgrades | Can spread cost long-term | Closing costs and mortgage changes |

For most homeowners, the best first step is not applying for financing right away. The best first step is getting a clear roofing estimate. Once we inspect the roof and explain the project scope, you can compare financing options using a real project number instead of guessing.

How Monthly Payments Are Calculated

Understanding monthly payments is critical before committing to any metal roof financing plan. Several factors influence how much you’ll pay each month, including the total project cost, interest rate, loan term, and type of financing chosen. For Greeneville, TN homeowners, having a clear picture of your monthly obligation helps ensure that a high-quality metal roof does not strain your household budget.

Factors That Affect Payments

- Total Project Cost – This includes metal panels, tear-off of old shingles, underlayment, flashing, trim, ridge caps, ventilation, labor, and permits. Storm damage or deck repairs can increase the total cost.

- Loan Amount – The principal borrowed directly affects the monthly payment. Higher loan amounts result in higher payments unless the term is extended.

- Interest Rate (APR) – Rates depend on credit score, lender type, loan type, and current market rates. A higher APR increases the monthly payment and total interest paid over time.

- Loan Term – Shorter terms lead to higher monthly payments but less total interest, while longer terms reduce monthly payments but increase total interest.

- Down Payment / Promotions – Some contractor financing offers 0% down or deferred-interest plans. These can lower initial payments but may carry risks if the balance is not cleared within promotional periods.

- Credit Profile – Lenders review your credit score, debt-to-income ratio, and financial history. Scores above 720 typically qualify for better terms, while 640+ may still receive financing at slightly higher rates.

Example Monthly Payment Scenarios

| Roof Cost | 5-Year Term | 7-Year Term | 10-Year Term |

| $15,000 | $290–$330 | $230–$270 | $180–$210 |

| $25,000 | $480–$520 | $350–$390 | $270–$310 |

| $35,000 | $670–$720 | $490–$540 | $380–$430 |

These examples assume an interest rate range of 6.99%–9.99% APR. Actual payments depend on the lender, the loan type, and the borrower’s profile.

Short-Term vs. Long-Term Financing

- Short-term loans: Higher monthly payment, lower total interest. Ideal for homeowners with strong cash flow who want to pay off the loan quickly.

- Long-term loans: Lower monthly payment, higher total interest. Beneficial if the monthly budget is tight, but be aware of the increased lifetime cost.

We can provide homeowners with accurate project estimates and show how different financing scenarios would affect monthly payments. This allows for better planning and helps avoid surprises once the loan is approved.

Approval Tips to Get the Best Rates

Securing the best possible loan terms requires preparation. Lenders evaluate creditworthiness, documentation, and debt-to-income ratio. Here are proven strategies to improve your approval chances:

Check Your Credit Score

- Homeowners with 720+ credit scores generally receive the most favorable APRs.

- Scores above 640 may still qualify, but may face higher rates or shorter terms.

- Review credit reports for errors and resolve discrepancies before applying.

Prepare Documentation

Commonly requested documents include:

- W-2 forms or tax returns

- Recent pay stubs

- Bank statements

- Government-issued ID

Having these ready can speed up approval and help qualify for the best offers.

Compare Multiple Financing Offers

- Contractor financing (Hearth, GreenSky, in-house plans)

- Personal loans or credit union offers

- HELOC or home equity loans

Compare APR, loan term, fees, monthly payment, deferred interest, and same-as-cash promotions.

Understand Your Debt-to-Income Ratio

- Lenders calculate the ratio of monthly debt obligations to gross income.

- Lower DTI improves chances for approval and may lead to better interest rates.

Prequalification

- Platforms like NerdWallet or LendingTree allow soft credit checks.

- Prequalification shows estimated rates and terms without affecting your credit score.

Contractor and Manufacturer Programs

- Some GAF-certified contractors or local Tennessee roofing companies offer exclusive financing plans.

- These plans may include perks such as 0% down, extended deferred interest, or bundled roofing services.

Financing with Insurance and Storm Repairs

Metal roofs are often replaced not only for aging or efficiency upgrades but also due to storm damage. Financing can help homeowners cover costs that insurance doesn’t fully pay for, such as deductibles or optional upgrades. Understanding how financing interacts with insurance claims is critical for Greeneville, TN, homeowners looking to protect their property and budget.

Using Financing for Deductibles or Upgrades

When a roof is damaged by hail, wind, or severe storms, homeowners may need immediate replacement to prevent leaks or further structural issues. While insurance may cover part of the cost, deductibles or upgraded materials may not be fully reimbursed. Financing provides the flexibility to pay for:

- Insurance deductibles

- Upgrades to standing seam or premium metal panels

- Additional protective measures like underlayment, ventilation, or high-gauge metal

We can provide a detailed roof inspection and estimate that homeowners can use to align financing with insurance coverage. This ensures you only borrow what is necessary while avoiding surprises during the insurance claim process.

Storm Damage Roof Replacement

Prompt roof replacement after storm damage is crucial. Delays can cause leaks, mold growth, and water damage to insulation, ceilings, and walls. Contractor financing allows homeowners to begin work immediately, rather than waiting to save for a full cash payment. A professional roofing company like Covenant Roofing & Restoration can handle inspections, provide accurate repair or replacement plans, and assist with the financing process, giving homeowners confidence and peace of mind.

Common Financing Mistakes to Avoid

Choosing the wrong financing approach can lead to higher long-term costs or project delays. Here are common mistakes to avoid:

- Focusing only on the monthly payment – Lower monthly payments often mean longer loan terms and higher total interest. Always compare the total loan cost.

- Ignoring deferred-interest clauses – Promotional 0% APR plans may charge full interest retroactively if the balance is not paid on time.

- Using high-interest credit cards for large roofing projects can increase the overall cost significantly if not paid off quickly.

- Signing before understanding the roofing scope – Ensure the estimate covers panels, underlayment, flashing, ventilation, and labor.

- Hiring an unqualified or uninsured contractor – Financing is only helpful if the roof is installed correctly. Check for licensed, insured, and GAF-certified contractors.

By avoiding these pitfalls, homeowners can secure financing that works for their budget and ensures a long-lasting, properly installed metal roof.

Why Greeneville Homeowners Should Choose Covenant Roofing & Restoration

Covenant Roofing & Restoration specializes in helping Greeneville homeowners navigate metal roof financing while ensuring high-quality installation. Here’s how they help:

- Roof Inspection and Estimates: Assess current roof condition and provide detailed cost estimates for metal panel replacement or repair.

- Material Guidance: Compare panel types, metal gauge, fasteners, and finishes to match home style and performance needs.

- Flexible Financing Options: Assist with contractor-backed financing, personal loans, HELOCs, and insurance-aligned funding.

- Professional Installation: Licensed and insured crews handle all roofing tasks including underlayment, flashing, and ventilation.

- Storm Damage Support: Evaluate damage, coordinate with insurance adjusters, and help homeowners finance any uncovered portion.

- Warranty Assurance: Ensure that installation meets manufacturer requirements for coverage.

Homeowners get not only the right financing plan but also a roof that protects their investment for decades.

Final Thought

Financing a metal roof is a practical way for Greeneville homeowners to protect their home, upgrade materials, and manage costs. By understanding loan options, monthly payments, approval tips, and insurance interactions, homeowners can choose a plan that fits their budget while ensuring a long-lasting roof.

Partnering with Covenant Roofing & Restoration ensures homeowners get: accurate estimates, guidance on financing options, professional installation, and support throughout the insurance and loan process. Whether upgrading after storm damage or investing in a premium metal roof, a well-planned financing strategy allows you to protect your home today while paying over time.