Summary: Before hiring a roofer in Greeneville, TN, verify their Tennessee contractor’s license through the Board for Licensing Contractors (required for projects over $25,000), confirm active general liability and workers’ comp insurance, and check for manufacturer certifications from GAF, Owens Corning, or CertainTeed. Get a line-item estimate with specific product names, understand the difference between material and workmanship warranties, and know how to spot storm chasers who show up uninvited after severe weather.

Table of Contents

When it comes to roofing, hiring the right professional is crucial for the safety and durability of your home. A bad roofing job can lead to expensive repairs, safety hazards, and even structural damage to your home. If you’re in Greeneville, Tennessee, and are planning to hire a roofing contractor, it’s important to ask the right questions before you commit.

Our roofers expert research these verified checkpoints, which will guide you through the essential questions to ensure that you hire a qualified, reliable, and trustworthy roofer who will deliver quality work.

1. Do They Actually Have a Tennessee Contractor’s License?

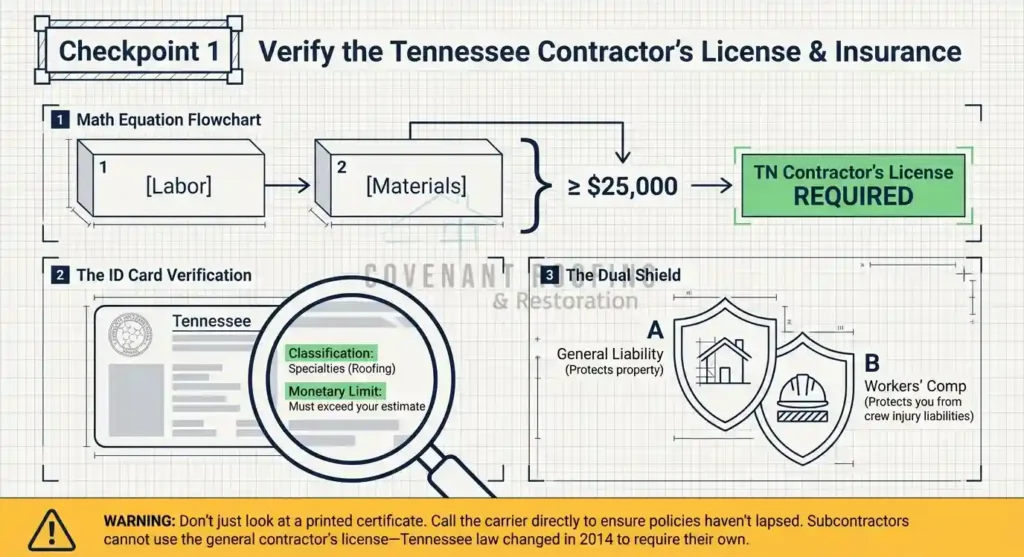

Most homeowners assume every roofer working in Tennessee carries a state roofing license. They don’t, because one doesn’t exist. Tennessee has no roofing-specific license. What the state requires is a contractor’s license issued by the Tennessee Board for Licensing Contractors, and only when the project hits $25,000 or more in combined materials and labor.

For a full roof replacement in Greeneville, you’re almost certainly crossing that $25,000 line. So if a contractor tells you they don’t need a license for your job, ask them to explain the math. And if they claim they’re “just a subcontractor,” that excuse stopped working in 2014, when Tennessee started requiring roofing subcontractors to carry their own contractor’s license too.

How to Verify a Tennessee Roofing Contractor’s License

You can check any roofer’s license directly on the Tennessee Board for Licensing Contractors.

Every license shows two things: a classification and a monetary limit.

Roofing falls under the “Specialties” classification. The monetary limit tells you the maximum project value that contractor is approved to bid on. If the number on their license is lower than your project estimate, they’re not legally qualified to take the job. If they can’t give you a license number on the spot, that tells you something too.

Why You Need to Check Their Insurance Yourself

Beyond licensing, ask for two documents: a general liability policy and a workers’ compensation policy.

General liability covers damage to your property during the work. Workers’ comp covers injuries to the roofing crew while they’re on your roof. Without workers’ comp, an injury on your property could land on your shoulders, and your homeowner’s insurance may not step in.

Don’t Just Look at the Certificate

A printed roofer certificate is easy to produce. What matters is whether the policy behind it is still active. Call the insurance carrier listed on the certificate and confirm the coverage is current. Policies lapse between renewals more often than you’d think, and a certificate from six months ago doesn’t guarantee anything today.

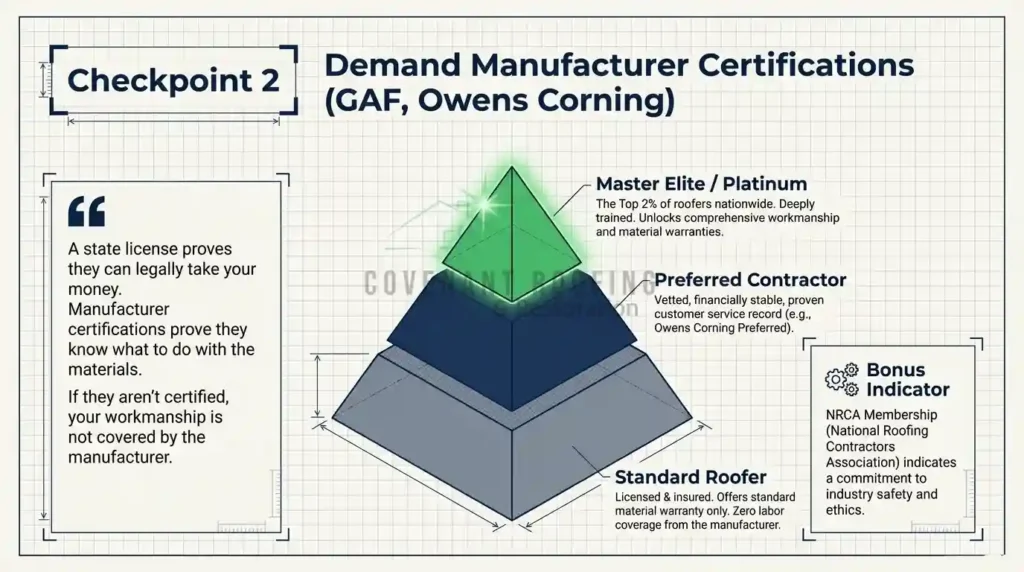

2. Manufacturer Certifications: GAF, Owens Corning, and What They Actually Mean

A Tennessee contractor’s license proves a roofer can legally take your money. Manufacturer certifications tell you whether they actually know what they’re doing with the materials going on your roof.

The three biggest names in residential roofing are GAF, Owens Corning, and CertainTeed. Each one runs its own contractor certification program, and each has multiple tiers.

Not all certifications are equal, and not every “certified” roofer has earned the same level of approval.

What These Certifications Actually Require

Owens Corning’s Preferred Contractor network, for example, requires at least $1,000,000 in general liability insurance, a financial stability screening, and a track record of customer service. Their Platinum tier adds additional training and performance requirements on top of that.

GAF’s Master Elite program is their highest tier. GAF says roughly 2% of roofing contractors nationwide hold that designation. Whether that exact number is marketing or math, the screening behind it is real: contractors have to be licensed, insured, and maintain a strong reputation to keep the status active.

CertainTeed runs a similar tiered system through their ShingleMaster and SELECT ShingleMaster programs, with training requirements that go deeper into product-specific installation techniques.

Why Certification Affects Your Warranty

Here’s where this gets practical. A certified contractor can typically offer you an extended warranty that covers both the roofing materials and the workmanship.

A non-certified contractor installing the exact same shingles? You’ll get the standard manufacturer’s material warranty and nothing more. The labor side won’t be covered.

That gap matters. If your roof leaks three years after installation because of a faulty install rather than a defective shingle, a material-only warranty won’t pay for the fix. A workmanship warranty backed by the manufacturer will.

Ask your roofer which manufacturers they’re certified with and what warranty tier that certification unlocks. If they can’t answer that question clearly, they either don’t hold the certification or don’t understand what it offers you.

What About NRCA Membership?

The National Roofing Contractors Association isn’t a certification in the same sense. It’s a trade association. But members agree to a code of ethics, and the organization provides ongoing training, safety standards, and best practice guidelines.

It’s not a dealbreaker if your roofer isn’t an NRCA member. But if they are, it tells you they’re plugged into the industry beyond just showing up and nailing shingles.

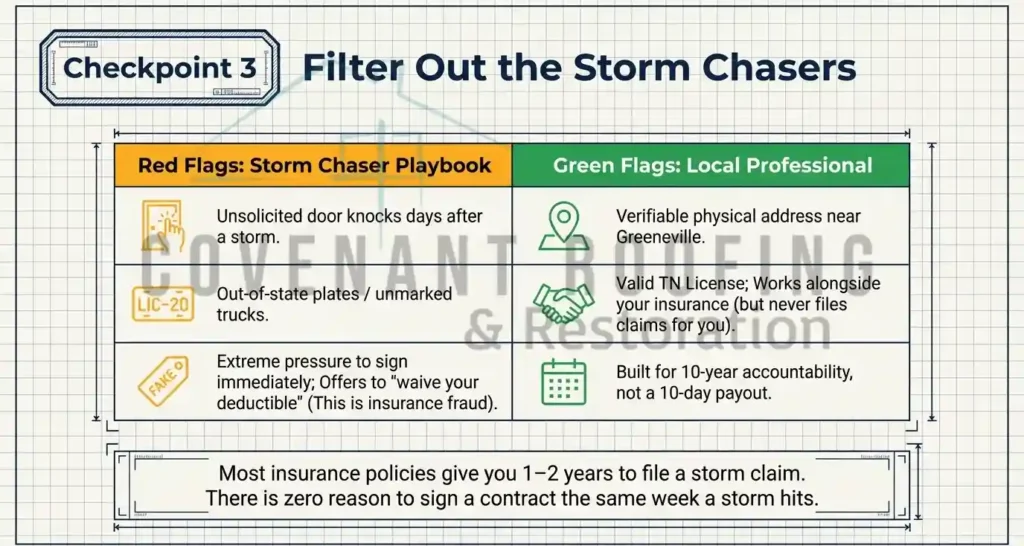

3. Storm Chasers vs. Local Roofers

Every time a big storm rolls through East Tennessee, a second wave follows right behind it. Not rain or wind, but out-of-state contractors in unmarked trucks, knocking on doors before the debris is even cleared.

These are storm chasers. Some are just aggressive salespeople. Others are outright scammers. Either way, they’re not here to build a relationship with you or your neighborhood. They’re here to close a deal and move on to the next storm.

How the Storm Chaser Playbook Works

The pattern is almost always the same. A contractor shows up at your door uninvited, usually within days of a major storm. They say they noticed damage on your roof while driving by, or that they were “just working on a neighbor’s house.”

They offer a free inspection. Once on the roof, they come back down with photos of damage and a sense of urgency. Sign today, they’ll say, before the price goes up or the schedule fills.

Some will offer to handle your entire insurance claim for you. Others will sweeten the deal by offering to cover your insurance deductible. That second one isn’t a favor. It’s insurance fraud, and it can put you, the homeowner, on the hook legally.

In the worst cases, contractors have been caught creating damage that wasn’t there. Cleated shoes on shingles, tools used to mimic hail impact. They photograph the “damage,” file an inflated insurance claim, collect the payout, and do the bare minimum work with the cheapest materials they can find.

What Happens After They Leave Town

Even when storm chasers do complete the job, the problems tend to show up later. Shingles that weren’t nailed to manufacturer spec blow off in the next windstorm. Flashing around chimneys and vents starts leaking within a year or two because it was rushed. Underlying deck rot gets covered up with new shingles instead of being repaired.

And when you try to call the company back? The phone number is disconnected. The “local office” was a rented space that’s already been vacated. The warranty they gave you is a piece of paper with no company behind it.

Manufacturer warranties can also get voided entirely if the installation was done by a contractor who wasn’t certified or licensed. So you’re left with a failing roof, no warranty, and no one to call.

Red Flags That Point to a Storm Chaser

A few things to watch for:

They showed up at your door unsolicited right after a storm. They can’t provide a physical business address in or near Greeneville. They pressure you to sign a contract before you’ve spoken to your insurance company. They offer to waive your deductible or “take care of” your claim. They can’t produce a verifiable Tennessee contractor’s license number. Their vehicles have out-of-state plates and no company branding.

Any one of these on its own is worth a pause. Two or more together, and you should walk away.

What to Do Instead After Storm Damage

Your first call after a storm should go to your insurance agent, not to whatever contractor knocked on your door. File the claim, let the adjuster come out and inspect the damage, and then get estimates from roofers you’ve actually vetted.

You have time. Most insurance policies give you one to two years to file a storm damage claim, depending on your carrier and plan. There is no reason to sign anything the same week a storm hits.

A local roofer with a physical office like Covenant Roofing & Restoration, a verifiable license, and years in the Greeneville community has something no storm chaser can offer: accountability. They’ll still be here when you need a callback two years from now.

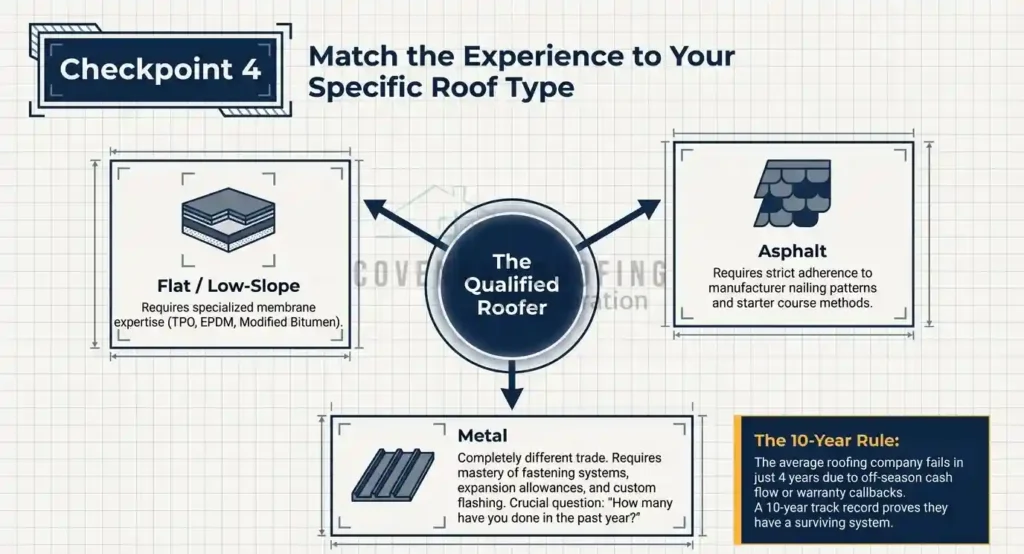

4. Experience and Roof Types: Matching the Roofer to Your Roof

Years in business gets talked about a lot when homeowners are comparing roofers. And it matters, but not in the way most people think. A company that’s been around for 15 years has survived slow seasons, supplier shortages, and the kinds of callbacks that teach you what not to do next time. A company that opened last spring hasn’t been tested yet.

But the age of the business is only part of the picture. The experience of the actual crew showing up to your house matters just as much. Some roofing companies have been around for decades but cycle through new, undertrained crews every season. Ask who will be on your roof, how long they’ve been with the company, and what kind of training they’ve gone through.

Why a 10-Year Track Record Matters More Than a Low Bid

The roofing industry has a high failure rate. The average roofing company lasts roughly four years, often because newer businesses don’t plan well enough to survive the off-season or handle the financial weight of warranty callbacks. A company that’s made it past the ten-year mark has dealt with enough installs, enough weather events, and enough customer issues to have a system in place.

That doesn’t mean a newer company is automatically bad. But it does mean you should dig deeper into their background. Did the owner work for another established roofer before starting out?

Does the crew have individual experience even if the company is new?

These questions fill in the gaps that “how long have you been in business” leaves open.

And if a roofer’s bid comes in significantly lower than everyone else’s, the experience question becomes even more relevant. Low bids usually mean one of three things: less experienced crews working faster, cheaper materials, or corners being cut on things you won’t notice until a year or two later.

Asphalt, Metal, or Flat: Does Your Roofer Actually Know the Difference?

Roofing isn’t one skill. It’s several, and the techniques change depending on the material.

Asphalt shingle installation is the most common in Greeneville and across East Tennessee. Most residential roofers are comfortable with it. But “comfortable” and “certified” aren’t the same thing. Ask whether they follow the manufacturer’s specific nailing pattern, how they handle the starter course, and what underlayment they use. These details separate a solid shingle job from one that starts failing after a few storm seasons.

Metal roofing is a different trade altogether. The fastening systems, expansion allowances, and flashing details on a standing seam metal roof have almost nothing in common with a shingle install. If you’re considering metal, ask how many metal roofs the contractor has completed in the past year. Not in their lifetime. In the past year. Recency matters because techniques and products change.

Flat or low-slope roofing (common on additions, porches, and some commercial buildings) requires yet another set of skills. TPO, EPDM, and modified bitumen each have their own installation requirements, and a roofer who’s great with shingles may have zero experience with membrane systems.

What About Specialty Features?

If your roof includes skylights, dormers, complex valley lines, or a chimney, those details add another layer of difficulty. Water tends to find its way in at transitions and penetrations, not in the middle of a clean field of shingles. Ask your roofer how they handle these areas specifically, and ask to see photos of similar work they’ve completed.

Storm Damage and Insurance Claims: What Your Roofer Should Handle for You

In Greeneville, storm damage is part of owning a home. Between spring thunderstorms, occasional hail, and high wind events, most roofs in the area will take a hit at some point during their lifespan.

A roofer with storm damage experience will know what to look for beyond what’s obvious from the ground. Granule loss on shingles, cracked flashing, lifted edges, soft spots on the deck. They’ll also know how to document it properly: before-and-after photos, written damage assessments, and a scope of work that matches what the insurance adjuster needs to see.

Should Your Roofer Talk to Your Insurance Company?

This is where it gets tricky. A good roofer can and should help you understand the damage and prepare documentation that supports your claim. They can meet with the adjuster on-site, walk the roof together, and make sure nothing gets missed.

But your roofer should never file the claim on your behalf or deal with your insurance company without your involvement. That’s your policy, your claim, and your responsibility. Any contractor who wants to “handle everything” with your insurer is either overstepping or setting up a situation you don’t want to be part of.

The best setup is a roofer who works alongside your insurance process, not one who tries to take it over.

5. The Estimate, the Materials, and What Should Be in Writing

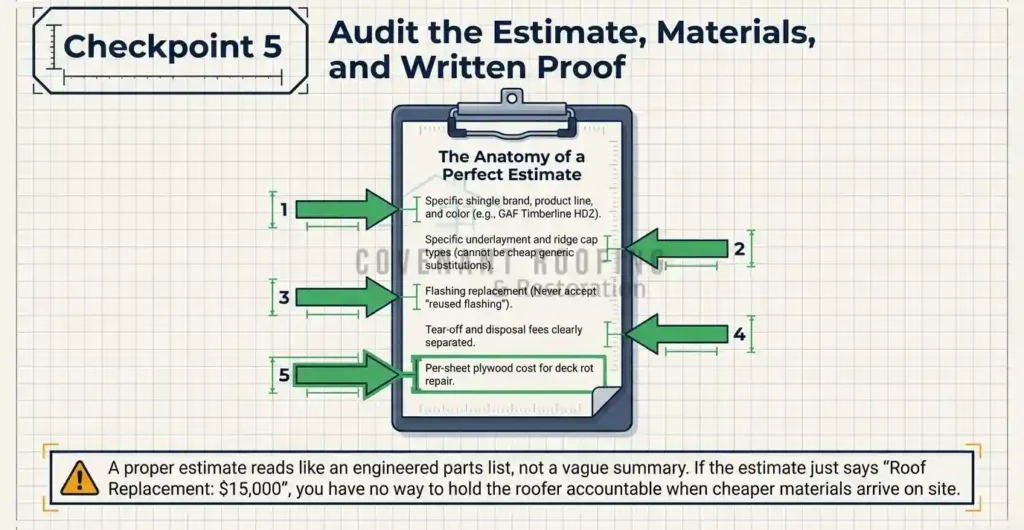

A roofing estimate should read like a parts list, not a summary. If the number at the bottom is the only thing that’s clear, the estimate isn’t doing its job. You need to see what you’re paying for, broken down by line item, before you agree to anything.

Line-Item Estimates: What Yours Should Actually Include

A proper estimate separates materials from labor and lists both with quantities and unit costs. You should be able to see the type of shingles, the number of squares being installed, the underlayment product, the flashing materials, ridge vents, drip edge, and any other components going on the roof. Labor should be its own line, not bundled into a vague total.

If the estimate just says “roof replacement” followed by a single dollar amount, you have no way to compare it against another contractor’s bid. You also have no way to hold the roofer accountable if cheaper materials show up on install day than what was discussed.

A few things that should also appear in the estimate but often don’t: the cost of tear-off and disposal of the old roof, permit fees if your municipality requires them, and a line for potential deck repair with a per-sheet price for plywood replacement. That last one matters because deck damage is the most common source of surprise costs on a roofing project, and a good estimate addresses it upfront rather than springing it on you mid-job.

What “Free Estimate” Actually Means?

Most roofing contractors in Greeneville offer free estimates, and that’s standard for the industry. But free doesn’t always mean thorough. Some estimates are based on a quick ground-level visual or a satellite measurement without anyone actually getting on the roof. Others involve a full inspection with photos and measurements taken from the roof deck.

Ask how the estimate will be prepared. A roofer who gets on the roof before quoting you a price is far more likely to catch issues that affect the final cost than one working from a screen.

Make Sure the Exact Materials Are in the Estimate

A roofer telling you they’ll use “architectural shingles” isn’t enough. The estimate should name the specific product line, the manufacturer, and the color or series. There’s a real difference between a GAF Timberline HDZ and a budget-tier architectural shingle from a lesser-known brand, even though both technically fall under the same category.

The same goes for underlayment, ridge caps, drip edge, and ice and water shield. These items might seem minor compared to the shingles themselves, but they affect how long the roof holds up and whether the manufacturer’s warranty stays valid. Many manufacturer warranties require that specific companion products are used alongside their shingles. If your roofer substitutes a cheaper underlayment to save a few dollars per square, it could void the warranty you thought you were getting.

What If the Roofer Wants to Change Materials Mid-Job?

Sometimes a roofer discovers during tear-off that the original material spec won’t work as planned. Maybe the deck condition requires a heavier underlayment, or a product is backordered and they want to substitute something comparable. That’s not automatically a problem, but the substitution should never happen without your written approval first.

Any material change should come with an updated line item in the estimate showing what’s being swapped, why, and whether it affects the cost or warranty coverage. If a roofer makes substitutions without telling you, you won’t know what’s actually on your roof until something goes wrong.

Deck Rot, Flashing, and the Stuff That Causes Leaks Later

The parts of a roof you can’t see after installation are usually the parts that fail first. Deck sheathing, flashing, and sealant work are where most leaks originate, and they’re also the areas most likely to get rushed or skipped by a contractor trying to finish fast.

Deck Inspection and Repair

The roof deck is the plywood or OSB sheathing underneath your shingles. Before a new roof goes on, the old roofing material comes off, and the deck should be inspected sheet by sheet. Any soft spots, water staining, or visible rot means that section needs to be replaced before the new materials go down.

A good roofer will tell you upfront that deck repair is a possibility and include a per-sheet replacement cost in the estimate. At Covenant Roofing, we photograph any rot we find and show it to homeowners before replacing the wood, so there’s no question about why the extra cost was added.

If your roofer’s estimate doesn’t mention the deck at all, ask what happens if they find damage once the old roof is off. You want that answer in writing before work starts, not delivered as a surprise phone call on day two.

Flashing and Sealing

Flashing is the metal (usually aluminum or galvanized steel) installed around roof penetrations like chimneys, skylights, vent pipes, and along valleys where two roof planes meet. Its only job is to direct water away from the seams where it would otherwise get in.

Bad flashing work is the single most common cause of roof leaks. Reusing old flashing to save time, cutting corners on step flashing along walls, or relying on caulk instead of proper counter-flashing around a chimney are all shortcuts that show up as water damage a year or two after installation.

Ask your roofer whether they plan to replace all flashing or reuse any existing pieces, and what type of ice and water shield they’ll install in valleys and around penetrations. These details don’t usually make it into a basic estimate unless you ask for them.

6. Timeline, Payment, and What Happens When Things Change

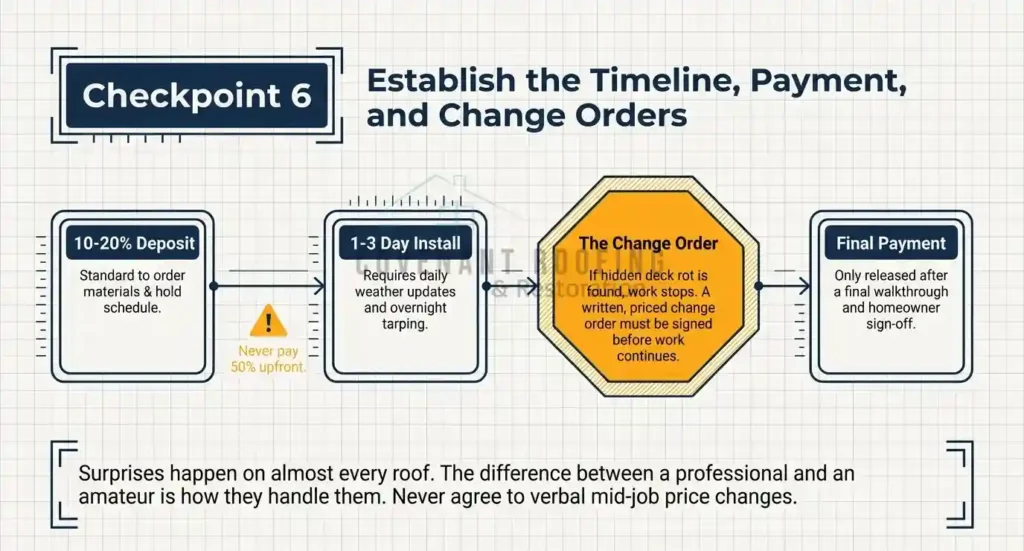

A roof replacement in Greeneville typically takes one to three days for a standard residential home, depending on the size of the roof, the material being installed, and the weather. But knowing the general range isn’t enough. You need specific dates, a clear payment structure, and a plan for what happens when something doesn’t go as expected.

How Long Will This Take, and What If It Rains?

Before signing anything, ask for a projected start date and a projected completion date.

Not a range. Not “sometime next week.” Actual dates.

Weather is the most common reason roofing projects in East Tennessee get delayed, especially during spring storm season. A good roofer won’t promise to work through rain. Shingles shouldn’t be installed on a wet deck, and adhesive strips on asphalt shingles won’t seal properly in cold or damp conditions. So delays happen, and that’s fine.

What matters is how the roofer communicates those delays to you. Ask upfront how they’ll keep you updated if the schedule shifts. Will they call you the morning of? Send a text the night before? Or will you just wake up to an empty driveway and no explanation?

Also ask about the crew’s daily schedule. What time do they start? What time do they wrap up? Will they tarp the roof at the end of each day if the job runs more than one day? An exposed, partially torn-off roof sitting overnight without protection is a problem waiting to happen.

Payment Terms: How Much Upfront Is Too Much?

Payment structures vary between roofing contractors, but a few things should raise your guard.

A deposit of 10 to 20 percent before work begins is standard in the industry. It covers the contractor’s material ordering costs and holds your spot on the schedule. Some contractors ask for a third upfront, which is on the higher side but not unusual for larger projects.

What isn’t normal: paying 50 percent or more before a single shingle has been removed. And paying the full amount before the job is complete should never happen, regardless of what the roofer tells you.

Get the Payment Schedule in the Contract

The payment terms should be spelled out in the contract, not agreed to verbally. You should see the deposit amount, when the next payment is due (usually at a specific project milestone like tear-off completion or material delivery), and when the final payment is expected (typically after a walkthrough and your sign-off that the job is done).

If a roofer asks for cash only or offers a discount for paying in cash, that’s a red flag. It could mean they’re trying to avoid a paper trail, and it leaves you with no proof of payment if a dispute comes up later.

What Happens When Unexpected Costs Come Up?

On almost every roofing project, something comes up that wasn’t in the original estimate. The most common one is deck damage that’s only visible once the old shingles are removed. But it could also be rotted fascia boards, damaged soffit, or additional flashing work around a chimney that looked fine from the outside.

The question isn’t whether surprises will happen. It’s how the roofer handles them when they do.

Change Orders: What They Are and Why You Need Them

A change order is a written document that describes the additional work, the reason for it, and the cost. It should be signed by both you and the contractor before the extra work begins. Not after. Not verbally agreed to while the crew is standing on your roof waiting for an answer.

Any roofer who does additional work without a signed change order is putting you in a position where you’ll argue about the bill at the end of the project. And at that point, you have very little leverage because the work is already done.

Ask your roofer during the estimate phase: “What’s your process if you find something unexpected?” If their answer is vague or amounts to “we’ll figure it out,” keep looking. The right answer involves documentation, your approval, and a clear cost before any extra work starts.

7. Material Warranty vs. Workmanship Warranty

Most homeowners hear “warranty” and assume they’re covered. But roofing warranties aren’t one thing. They’re two separate agreements from two different parties, and they cover two different types of failure. Confusing them, or not asking about both, can leave you paying out of pocket for a problem you assumed was covered.

What a Material Warranty Covers

A material warranty comes from the shingle or roofing product manufacturer, not your contractor. It covers defects in the product itself. If a shingle cracks, curls, or fails prematurely due to a manufacturing flaw, the manufacturer will cover replacement materials under the terms of the warranty.

Most architectural shingle warranties run 30 years to lifetime, depending on the product line. Three-tab shingles typically carry 20 to 25 year coverage. Metal roofing warranties can stretch to 40 or 50 years on premium standing seam systems.

But the fine print matters. Many material warranties are prorated, meaning the coverage decreases over time. A “lifetime” warranty that’s heavily prorated after year 10 isn’t worth nearly as much as it sounds. Ask your roofer to walk you through the actual terms, not just the headline number.

What Voids a Material Warranty

Manufacturer warranties often come with conditions that homeowners don’t find out about until it’s too late. Common ones include:

Installation by a non-certified contractor. If the manufacturer requires a certified installer and your roofer doesn’t hold that certification, the warranty may be void from day one.

Improper ventilation. Most shingle manufacturers require that the attic below the roof meets specific ventilation standards. If it doesn’t, and the shingles fail because of heat buildup, the claim gets denied.

Failure to use the manufacturer’s recommended companion products. If your roofer used a third-party underlayment or a generic ridge cap instead of the manufacturer’s specified system, that can be enough to void coverage.

Ask your roofer directly: “Is there anything about this installation that could void the manufacturer’s warranty?” If they can’t answer that question with specifics, they may not know the warranty requirements well enough to protect your coverage.

What a Workmanship Warranty Covers

A workmanship warranty comes from the roofing contractor, not the manufacturer. It covers errors in installation. If a leak develops because the flashing was installed wrong, the nailing pattern was off, or the starter course wasn’t properly sealed, a workmanship warranty means the contractor comes back and fixes it at no charge to you.

Workmanship warranty lengths vary widely. Some contractors offer one year. Others offer five or ten. A few manufacturer certification programs (like GAF’s Golden Pledge or Owens Corning’s Platinum Protection) extend workmanship coverage to 25 years or more, backed by the manufacturer rather than the contractor alone.

The length of the warranty matters, but so does who’s standing behind it. A 10-year workmanship warranty from a company that’s been in Greeneville for 15 years carries more weight than a 10-year warranty from a company that opened six months ago. If the company folds in year three, your warranty goes with it.

Is the Warranty Transferable?

If you plan to sell your home at any point, this question matters. A transferable warranty means the coverage passes to the new homeowner when you sell. Not all warranties transfer automatically. Some manufacturers require the original homeowner to register the warranty within a specific window after installation (often 30 to 60 days), and then follow a separate transfer process at the time of sale.

A transferable warranty with remaining coverage adds real value to your home during a sale. A buyer looking at two similar houses, one with an eight-year-old roof and no warranty and one with an eight-year-old roof and 22 years of transferable coverage, is going to weigh that difference.

Ask your roofer three things about transferability: Does the material warranty transfer? Does the workmanship warranty transfer? And what paperwork needs to happen to keep both valid?

8. Cleanup, Nail Sweeps, and Protecting Your Yard

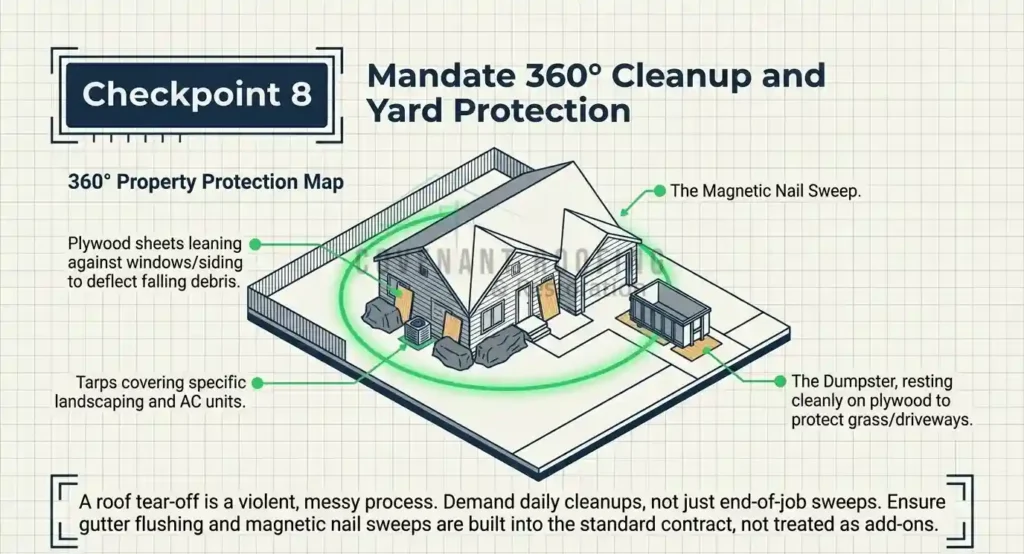

A roof replacement is one of the messiest jobs that can happen to the outside of your home. Old shingles, torn underlayment, bent flashing, exposed nails, packaging, and dust. All of it ends up somewhere, and if your roofer doesn’t have a plan for managing it, that somewhere is your lawn, your driveway, your flower beds, and your gutters.

What Should Be Protected Before Work Starts

Before the first shingle gets pulled, your roofer should have a protection plan for the areas around your home. That usually means tarps over landscaping, plywood sheets leaned against the side of the house to shield siding and windows from falling debris, and clear communication about where the dumpster will be placed.

Air conditioning units, outdoor furniture, grills, and vehicles should be moved or covered. If you have a garden or recently planted landscaping near the house, mention it before work begins. Most crews will work around it if they know about it, but they won’t notice it on their own in the middle of a tear-off.

Ask your roofer specifically what steps they take to protect the property. If the answer is vague or amounts to “we’re careful,” push for details. Careful doesn’t mean much when a 30-pound bundle of old shingles slides off the roof edge.

Nail Sweeps and Debris Removal

Roofing nails end up everywhere during a tear-off. In the grass, on the driveway, in flower beds, wedged between patio stones. A single missed nail can puncture a tire, injure a pet, or end up in a bare foot weeks after the job is done.

A professional crew will use a magnetic roller (sometimes called a nail magnet or magnetic sweeper) across the entire perimeter of the house after the job is complete. Some crews run it daily during multi-day projects, which is the better approach since nails scatter further than you’d expect when they’re being pulled from a roof two stories up.

Ask whether the nail sweep is part of their standard cleanup process or something you need to request separately. It should never be an add-on. It should be automatic.

What About the Gutters?

Gutters collect a surprising amount of debris during a roof replacement. Granules from old shingles, small pieces of underlayment, roofing cement, and dirt all wash into the gutter system during tear-off and installation. If the crew doesn’t flush or clean the gutters as part of the final cleanup, you could end up with clogged downspouts the next time it rains.

Ask whether gutter cleaning is included in the scope of work. If it isn’t, you’ll either need to do it yourself or hire someone separately, so it’s better to know that upfront.

Daily Cleanup vs. End-of-Job Cleanup

There’s a difference between a crew that cleans up once at the end of the project and one that cleans up at the end of every workday. On a multi-day job, daily cleanup matters. It keeps your property safer, reduces the chance of nails or debris causing damage overnight, and shows that the crew takes the worksite seriously.

Ask your roofer whether they do daily cleanup or just a final sweep. If the job is expected to take more than one day, daily cleanup should be the standard, not a special request.

The dumpster should also be positioned thoughtfully. Ideally, it sits on the driveway or street, not on your lawn. If it has to go on grass, the roofer should place plywood underneath to prevent the weight from tearing up the turf. Small detail, but it tells you a lot about how the crew treats your property.

9. Cheapest Quote vs. Best Value: How to Compare Roofers

Getting three quotes is solid advice. But three different numbers mean nothing if the scope behind them isn’t the same.

Why the Lowest Quote Usually Isn’t the Best Deal

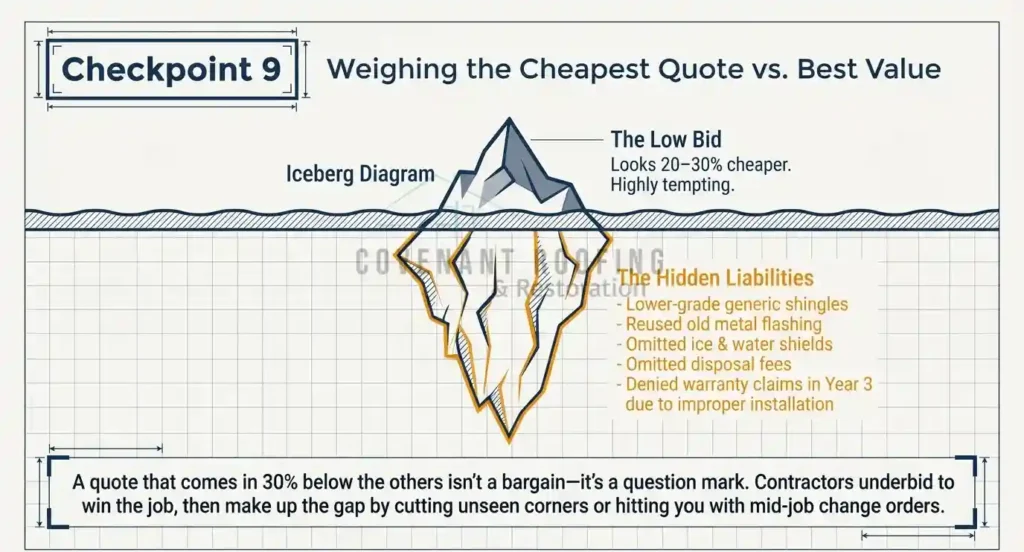

A quote that comes in 20 or 30 percent below the others isn’t a bargain. It’s a question mark. Something is different in that estimate, and you need to find out what.

Common reasons a bid comes in low: lower-grade shingles, reused flashing instead of new, no ice and water shield in the valleys, or tear-off and disposal not included. Some contractors underbid intentionally to win the job, then make up the gap with change orders once your old roof is already in the dumpster.

A higher quote with better materials and a stronger warranty will almost always cost less over the life of the roof than a cheap install that starts leaking in year five.

How to Compare Quotes Side by Side

Make sure every quote covers the same scope before comparing the price. Check each one for: the specific shingle brand and product name, underlayment type, whether flashing is being fully replaced or reused, ice and water shield placement, ventilation plan, tear-off and disposal, deck repair pricing, and warranty details for both materials and workmanship.

If a quote is missing more than one or two of those details, ask the contractor to fill in the gaps. A number without the specifics behind it tells you nothing.

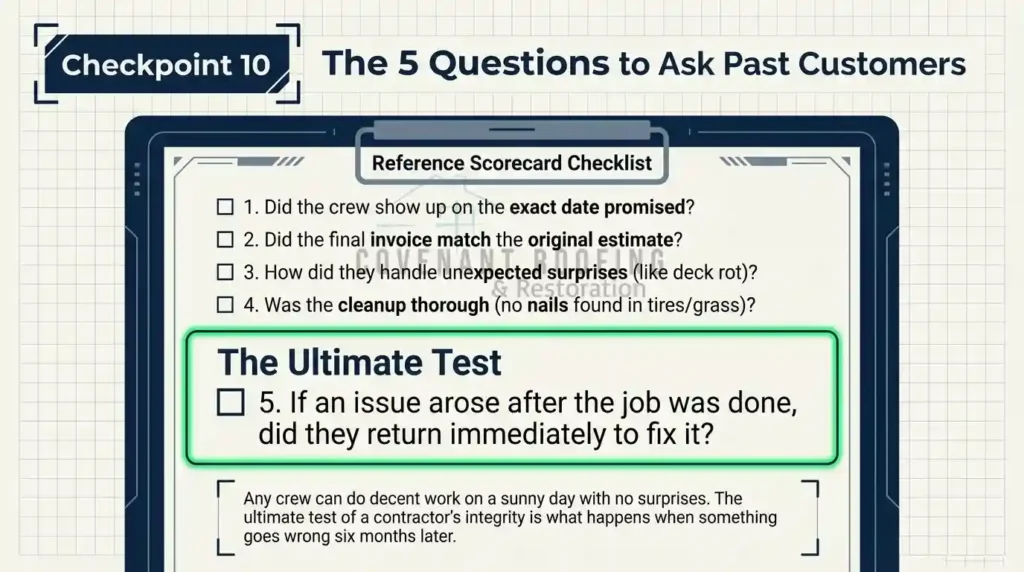

10. What to Ask a Roofer’s Past Customers?

Any roofer can tell you they do great work. Their past customers are the ones who can actually confirm it. Ask for references, and then actually call them. Most homeowners skip this step, and it’s the one that tells you the most.

What to Ask When You Call a Reference

Keep it simple and direct. A few questions will tell you most of what you need to know:

Did the crew show up on the date they promised? Did the final cost match the original estimate, or did it climb? How did the roofer handle anything unexpected that came up during the job? Was the cleanup thorough, or did you find nails and debris afterward? If you had an issue after the job was done, did they come back and take care of it?

That last question is the most revealing one. Any crew can do decent work on a sunny day with no surprises. What separates a good roofer from a bad one is what happens when something goes wrong six months later.

Ready to Ask These Questions? Start With Us

At Covenant Roofing and Restoration, we’ve built our business in Greeneville on the idea that an informed homeowner makes the best customer. We don’t dodge questions. We welcome them.

We carry a valid Tennessee contractor’s license, full general liability and workers’ compensation insurance, and manufacturer certifications that back up the warranties we offer. We provide line-item estimates before work begins, photograph any deck damage before replacing it, and we don’t ask for full payment until you’ve walked the finished job and signed off on it.

Call us or stop by our office in Greeneville to schedule an inspection.