Dealing with roof damage, especially after a storm or hail event, can be stressful, but having a roof insurance claim can alleviate some of that burden. Whether you’re facing hail damage, wind damage, or storm damage, knowing how to navigate the claims process is crucial for a smooth and successful outcome. In Tennessee, the weather can often lead to roof damage, making it essential for homeowners in places like Greeneville, TN to be prepared. This guide will walk you through the entire process of filing a roof insurance claim, helping you understand the steps, avoid common mistakes, and ensure you’re fully covered. Covenant Roofing is here to help you with professional roof inspections and insurance claims assistance.

Key Terms You Should Know Before Filing a Roof Insurance Claim in Tennessee

Before you begin the process, it’s important to understand the roofing terminology used in your policy.Knowing these terms will help you fully comprehend your policy and the insurance claim process.

Actual Cash Value (ACV)

Actual Cash Value (ACV) is the value of your roof after depreciation. For example, if your roof is 10 years old and has a 20-year expected lifespan, ACV will take into account the wear and tear over those 10 years. This can impact your settlement, as you’ll receive less than the full cost of replacement.

Replacement Cost Value (RCV)

Replacement Cost Value (RCV) is the amount it would take to replace your roof with new materials, without accounting for depreciation. This is often a more favorable option for homeowners, as it provides a more comprehensive payout for roof replacement, ensuring that your roof can be fully replaced rather than patched up.

Deductible

The deductible is the amount you need to pay out of pocket before your insurance company covers the rest. For example, if your roof damage is worth $10,000, and your deductible is $1,000, your insurance will pay $9,000. Understanding your deductible is crucial for managing your expectations when filing a claim.

Premium

Your premium is the amount you pay annually to keep your insurance policy active. The premium will vary based on factors like the value of your home, the type of coverage, and the deductible you choose.

Named Perils vs. Open Perils

Named perils are specific types of damage listed in your policy (e.g., wind, hail, fire). If a damage type is not listed in your policy, it is not covered. Open perils, on the other hand, provide broader coverage, covering all types of damage except those explicitly excluded. Open perils generally offer more comprehensive protection but may come with a higher premium.

Tennessee-Specific Terms

Tennessee residents should be aware of state-specific laws, such as the Matching Law, which requires insurance companies to pay for full roof replacement if the damaged shingles cannot be matched with existing ones. This ensures your roof maintains its appearance and functionality. Additionally, Act of God clauses often cover weather-related damage like storms or flooding, but these may require specific riders in your policy.

What Roof Damage Is Typically Covered by Insurance in Tennessee?

Understanding what is covered by your homeowner’s insurance policy is essential for filing a roof insurance claim. Roof damage due to severe weather or other incidents is usually covered, but there are exceptions that homeowners should be aware of. In Tennessee, damage caused by storms, hail, and wind is common and typically covered under a standard homeowner’s policy.

Storm Damage

Roof damage caused by severe storms is one of the most common reasons for filing a roof insurance claim. This can include wind damage, hail, or other weather-related issues. Hail can crack or dent shingles, while high winds can tear them off, leading to water infiltration and further structural damage. Since Tennessee experiences frequent storms, having comprehensive storm damage coverage is crucial. If a major event has compromised your home, our storm damage restoration team can help stabilize the structure and assist with the claims process.

Hail and Wind Damage

Hail storms can cause significant damage to roofs, especially if they involve large hailstones. Similarly, wind damage from thunderstorms or tornadoes can rip off shingles or even cause structural issues with your roof. Both hail and wind damage are typically covered by insurance policies, provided you can demonstrate that the damage was caused by a covered peril.

Fire and Vandalism

Damage from fire, vandalism, or other unexpected events is also typically covered by homeowner’s insurance. If your roof catches fire or is damaged due to criminal activity, your insurance should help pay for repairs or replacement. Coverage will vary depending on your policy, so it’s important to check the specifics.

Tree and Fallen Debris Damage

In Tennessee, fallen trees or branches from storms are a common cause of roof damage. Whether it’s from a severe windstorm or a heavy snowstorm, if a tree or large branch falls onto your roof, causing damage, insurance should cover the costs of repair or replacement. Many homeowner’s policies include this type of coverage, but it’s worth reviewing your individual policy.

Water Stains and Leaks

Roof leaks caused by storms are typically covered by insurance as long as the leaks are due to sudden damage (like wind tearing off shingles). Over time, leaks caused by normal wear and tear or poor maintenance might not be covered. It’s crucial to make sure that the damage is recent and related to a covered incident like a storm.

What Roof Damage Is NOT Covered by Insurance?

While roof insurance claims can cover a wide range of damage, certain types of damage typically aren’t covered by most homeowner’s policies. It’s important to know what your policy excludes to avoid surprises when filing a claim.

Wear and Tear

Most insurance policies do not cover wear and tear from aging roofs. If your roof is simply old and has deteriorated over time, this won’t typically be covered by insurance. Roofs have a finite lifespan, and after a certain point, the responsibility for repairs and maintenance shifts to the homeowner.

Cosmetic Damage

Minor cosmetic damage that doesn’t affect the roof’s functionality, such as small dents or discoloration, is usually not covered by insurance. For example, if your shingles are slightly damaged but do not cause leaks or other structural issues, this is typically considered cosmetic damage.

Neglect and Lack of Maintenance

If damage to your roof is the result of neglect or lack of maintenance, such as clogged gutters or missing shingles, your insurance may not cover the repairs. Homeowners are responsible for maintaining their roof and ensuring that issues are addressed before they become major problems.

Flood or Earthquake Damage

Most standard homeowner’s insurance policies do not cover flood damage or earthquake damage unless you have specific riders or additional coverage. In Tennessee, where flooding can occur, it’s essential to have flood insurance if you’re in a flood-prone area. Earthquake damage is also typically excluded unless you have earthquake insurance.

Step-by-Step Guide to Filing a Roof Insurance Claim in Tennessee

Now that you understand the key terms and what’s typically covered by insurance, it’s time to walk through the actual steps involved in filing a roof insurance claim. Whether you’ve experienced storm damage, hail damage, or wind damage, following these steps will help ensure you submit a complete and accurate claim to your insurance provider.

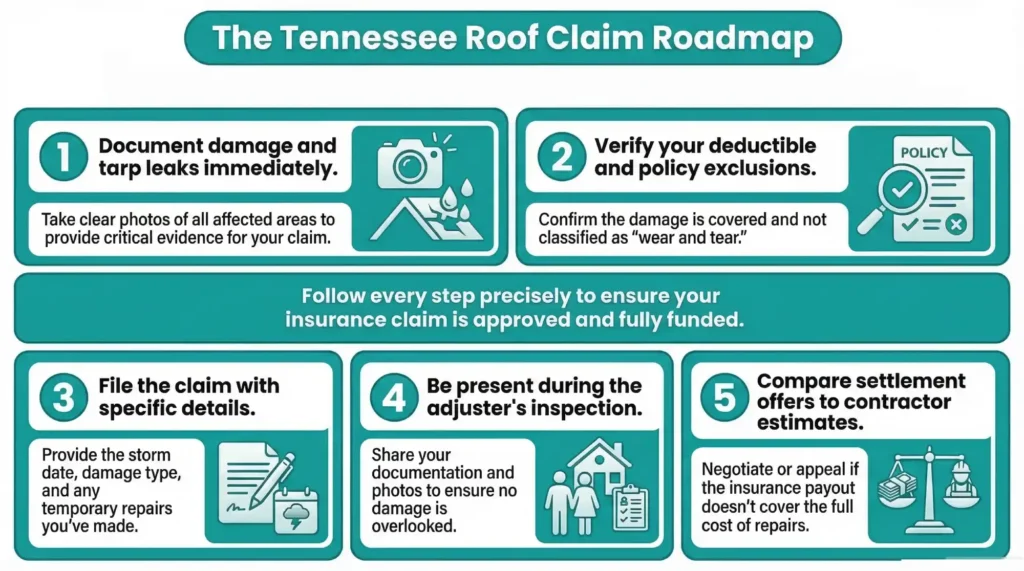

Step 1: Inspect Your Roof and Document the Damage

The first thing you need to do is identify the damage. If you’ve just lived through a severe weather event, you should immediately check for roof damage after a storm. If you’re not comfortable climbing onto your roof, it’s best to call a professional roofer who can perform a professional roof inspection. An experienced roofing contractor will be able to assess the full extent of the damage and ensure that nothing is overlooked.

Once you’ve identified the damage, be sure to take clear photos of all affected areas. These photos will serve as critical evidence for your insurance claim, especially if there are water stains or leaks caused by the damage. Documenting your roof damage as soon as possible helps to avoid potential delays in filing the claim and provides proof of the storm’s impact on your roof.

If your roof leaks, it’s essential to tarp the area temporarily to prevent further damage to your home’s interior while waiting for the insurance adjuster’s inspection. Many insurance companies require that temporary repairs be made immediately after the damage occurs to avoid further losses.

Step 2: Review Your Homeowner’s Insurance Policy

Before filing your claim, take a moment to carefully review your homeowner’s insurance policy. Look for specifics on coverage related to roof damage caused by storms, hail, and wind. Make sure to understand your deductible, which is the amount you’ll pay out-of-pocket before your insurance kicks in. The deductible amount can vary depending on your policy, so it’s important to know this before proceeding with the claim.

Additionally, check for exclusions in the policy. For example, some policies may exclude damage caused by wear and tear or lack of maintenance, so it’s important to be sure that the damage you’re claiming is covered. If you’re unsure about any aspects of your policy, it’s always a good idea to reach out to your insurance agent for clarification.

Step 3: Contact Your Insurance Company

After reviewing your policy and inspecting your roof, it’s time to contact your insurance company. You can typically file a claim by phone or online, depending on the provider. Be ready to provide details about the damage, including:

- The date and time the damage occurred (such as after a specific storm or event).

- The type of damage (e.g., hail damage, wind damage, or fallen tree damage).

- The steps you’ve taken to mitigate further damage, such as tarping the roof.

Once you’ve submitted your claim, your insurance provider will likely assign an insurance adjuster to inspect the roof and determine the extent of the damage. At this point, it’s important to keep records of all your communications with the insurance company, including emails, phone calls, and claim numbers.

Step 4: Schedule an Inspection with the Insurance Adjuster

Your insurance company will assign an adjuster to evaluate the roof damage. The adjuster will visit your property to assess the extent of the damage and determine the payout for your claim. It’s crucial to be present when the adjuster inspects your roof. This way, you can provide them with the documentation you’ve collected, including photos and inspection reports, and point out any damage they might have missed.

During the inspection, the adjuster will evaluate factors such as the severity of the damage, whether it is consistent with storm-related issues, and the overall condition of your roof. The more information you provide, the more accurate the insurance company’s evaluation will be.

Step 5: Review the Insurance Offer

Once the adjuster has completed their inspection, your insurance company will make an offer for the roof repairs or replacement based on their assessment. It’s important to review this offer carefully to ensure that it covers the full scope of the damage. If you feel the offer is insufficient or doesn’t fully cover the repairs, you have the right to negotiate.

At this stage, you may also want to get an independent roofing contractor’s estimate to compare with the insurance offer. If the insurance company’s settlement doesn’t meet the actual cost of the repairs, you can appeal the decision or request a supplemental claim for the difference.

Common Mistakes to Avoid When Filing a Roof Insurance Claim

Filing a roof insurance claim may seem straightforward, but many homeowners make common mistakes that can delay the process or result in less-than-ideal settlements. Here are the most frequent errors to avoid:

Mistake 1: Not Documenting the Damage Thoroughly

One of the most common mistakes homeowners make is failing to document the damage properly. Insurance claims require clear, detailed documentation of the damage to support your claim. Without this, the insurance company may not approve your claim, or they might offer a lower settlement. Always take clear photos and videos of the damage from multiple angles. If possible, include photos of the roof before the damage occurred.

Mistake 2: Delaying the Claim

Another mistake homeowners make is delaying the filing of their insurance claim. Insurance companies often have a specific window of time during which claims must be filed. If you wait too long, your claim could be denied, even if the damage was covered under your policy. Filing the claim immediately after the damage occurs ensures that you meet any deadlines and prevent complications later on.

Mistake 3: Failing to Hire a Professional Roofer for Inspection

While you may feel confident inspecting your own roof, professional roof inspections are crucial. Roofing professionals are trained to identify damage that may not be immediately visible to an untrained eye. They also know how to document the damage correctly, which will strengthen your claim.

Mistake 4: Ignoring the Fine Print of the Policy

Many homeowners don’t fully understand their insurance policy, leading to confusion and disappointment when their claim is processed. Before filing a claim, review the details of your policy, including coverage limits, exclusions, and deductible amounts. Knowing what is and isn’t covered will help you manage expectations and ensure that you’re not caught off guard.

Mistake 5: Accepting the First Offer Without Question

Insurance companies may offer you a settlement quickly, but that doesn’t mean it’s the best offer. Often, their first offer is lower than what you may be entitled to. Don’t hesitate to negotiate or seek a second opinion from a trusted roofing contractor. If you feel the initial offer is too low, request a supplemental claim or file an appeal.

Pro Tips for Filing a Successful Roof Insurance Claim in Tennessee

To maximize your chances of a successful roof insurance claim in Tennessee, follow these pro tips:

Tip 1: Hire a Professional Roofing Company

Work with a certified roofing contractor who specializes in insurance claims. A professional roofer will not only provide an accurate inspection but can also help you document the damage properly. They can act as an advocate when dealing with the insurance company, ensuring you get the coverage you deserve.

Tip 2: Document Everything

From phone calls with your insurer to inspection reports and photos of the damage, documentation is crucial. Keep a file with all related materials, as it will be your evidence if you need to negotiate or appeal.

Tip 3: Get a Second Opinion

If you’re unsure about the insurance adjuster’s evaluation, don’t hesitate to get a second opinion. A different roofing company may provide a more accurate assessment and help identify damage the insurance company missed.

Tip 4: Understand Your Deductible

Be sure to fully understand your deductible and how it impacts your payout. For example, if your deductible is high, it may affect how much you get reimbursed for repairs. Knowing this beforehand can help you plan your finances accordingly.

What to Do If Your Roof Insurance Claim Is Denied

Filing a roof insurance claim can sometimes lead to unexpected outcomes, including the possibility of your claim being denied. While it can be frustrating, it’s important to know that a denied claim doesn’t have to be the end of the process. There are steps you can take to challenge the decision and get the compensation you deserve.

Common Reasons for Claim Denial

There are several common reasons why an insurance company might deny a roof claim. Understanding these reasons will help you address the issue and possibly resolve it:

- Policy Exclusions: If the damage falls under an exclusion in your policy, like wear and tear or damage caused by lack of maintenance, your claim could be denied.

- Insufficient Documentation: If you didn’t provide enough evidence or photos to support your claim, the insurance company might deny it. Detailed documentation is essential.

- Missed Deadlines: Insurance companies often have time limits for filing claims, usually within a certain period after the damage occurs. Missing these deadlines can result in a denial.

- Failure to Mitigate Damage: If you didn’t take immediate steps to prevent further damage (such as tarping the roof), the insurance company may argue that the damage could have been minimized.

- Disagreements on Coverage: If your roof has aged or has pre-existing damage, your insurer might argue that it wasn’t storm damage but a result of general wear and tear, leading to a claim denial.

How to Appeal a Denied Roof Insurance Claim

If your claim is denied, don’t panic. You have the right to appeal the decision. Here are the steps to follow if you want to challenge the insurance company’s denial:

- Review the Denial Letter: Carefully read the denial letter to understand why the claim was rejected. This will help you address the specific reasons for the denial.

- Provide Additional Evidence: If your claim was denied due to lack of documentation, provide additional evidence, such as photos, reports, and invoices from roofing inspections. If the damage was not adequately assessed by the adjuster, ask for a re-evaluation.

- Request a Second Opinion: It may help to get a second opinion from a certified roofing contractor. A roofer experienced in insurance claims can assess the damage from a professional perspective and provide a more accurate report for your appeal.

- Hire a Public Adjuster: If you’re having difficulty navigating the appeal process on your own, you may want to hire a public adjuster. A public adjuster works on your behalf to ensure you get the proper settlement from the insurance company. They have the expertise to negotiate and fight for your claim.

- Contact Your Insurance Company: If you disagree with the initial decision, reach out to your insurance provider to ask for an appeal or reconsideration. In some cases, a simple conversation can lead to a re-assessment of the claim.

Covenant Roofing Can Help You With Denied Claims

At Covenant Roofing, we understand the challenges homeowners face when filing roof insurance claims. If your claim is denied, our team of certified roofing professionals is here to assist you. We can provide you with a detailed second opinion, assist with re-documentation, and help navigate the appeals process. Contact us to schedule a consultation, and let us help you ensure you get the compensation you deserve.

How Covenant Roofing Can Help You With Your Roof Insurance Claim

Filing a roof insurance claim can feel like a daunting task, but you don’t have to go through it alone. At Covenant Roofing, we offer comprehensive services to support you every step of the way. Here’s how we can assist:

Professional Roof Inspections

One of the most important aspects of filing a roof insurance claim is having a professional roof inspection. At Covenant Roofing, we provide thorough inspections to assess the damage accurately. Our roofing experts are trained to spot even the most subtle signs of damage that might be overlooked by a general contractor or insurance adjuster. With our detailed reports and high-quality photos, we help ensure that your insurance company sees the full scope of the damage.

Documentation Assistance

When filing an insurance claim, documentation is key. Our team can assist you in documenting the damage properly. We will take photos, provide written assessments, and help you compile all the necessary evidence to submit with your claim. Having professional documentation increases the chances of your claim being approved and ensures that the settlement you receive reflects the true cost of repairs or replacement.

Claims Assistance

Once the insurance company has assigned an adjuster to your claim, we can be there to assist you throughout the process. We’ll help you prepare for the adjuster’s inspection, answer any questions they may have, and ensure that all damage is fully documented. If necessary, we can provide additional estimates to help you negotiate a fair settlement. Our experience in working with insurance claims gives us the expertise to guide you through the process smoothly.

Roof Repairs and Replacement

After your insurance claim has been approved, Covenant Roofing is here to handle the roof repairs or replacement. Our team is committed to providing high-quality service and ensuring that the job is done right. Whether your roof needs a minor repair or a full replacement, we have the skills and resources to get the job done promptly.

Emergency Services

In the event of sudden roof damage, we also offer emergency roof tarping services to prevent further damage. Protecting your home from water leaks and additional damage is critical while your insurance claim is processed, and we can assist with temporary repairs to give you peace of mind.

Frequently Asked Questions About Roof Insurance Claims

What type of roof damage is covered by homeowners’ insurance?

Most homeowner’s insurance policies cover damage caused by storm damage, hail damage, wind damage, and fallen trees. Some policies may also cover fire damage or vandalism. However, general wear and tear or maintenance issues are typically not covered.

How long do I have to file a roof insurance claim in Tennessee?

You should file your claim as soon as possible after the damage occurs. Insurance companies typically require claims to be filed within a certain period, usually within one year of the incident. Always check your policy for specific deadlines.

Can I choose my own roofing contractor for insurance claims?

Yes, you can choose your own contractor for repairs or replacement. However, the insurance company may recommend contractors or have a network of preferred providers. Regardless, you have the right to hire any qualified licensed roofing contractor.

How do I know if my roof damage is covered under my homeowner’s insurance policy?

Review your policy carefully to understand your coverage limits and exclusions. If you’re unsure, reach out to your insurance company for clarification. Your roofing contractor can also help you determine if the damage qualifies for coverage.

What should I do if my roof insurance claim is denied?

If your claim is denied, first ask the insurance company for an explanation. Review the denial letter and ensure that you’ve provided all the necessary documentation. If you disagree with the decision, you can appeal the denial and provide additional evidence, or consider hiring a public adjuster to assist you.