When severe storms, hail, or high winds hit Greeneville, TN, the damage to your home can be overwhelming and stressful. Whether it’s your roof, siding, windows, or personal property like appliances and electronics, improperly documenting storm damage can result in denied or delayed insurance claims. The key to protecting your home and getting a fair settlement starts with structured, thorough, and timely documentation. This guide helps you capture every critical detail safely and efficiently, ensuring that insurance adjusters have all the information they need to process your claim accurately. If you want expert help, Covenant Roofing offers professional storm-damage inspections and documentation services for homeowners in Greeneville, TN.

Safety First: PPE and Hazard Awareness

Before inspecting your property, safety must be your top priority. Storm-damaged homes can hide hazards such as live electrical wires, gas leaks, unstable structures, or contaminated floodwater. Always use personal protective equipment (PPE), including gloves, boots, heavy clothing, and an N-95 respirator or mask to protect against dust, mold, or debris. A flashlight is essential for inspecting dark areas such as attics or under damaged ceilings.

If you need to use a portable generator, place it outside and away from your home to avoid carbon monoxide exposure. Do not attempt to enter areas that are structurally unsafe or show signs of flooding or fire hazards. These steps are not just recommendations; they are necessary to prevent injury and ensure you can safely document all storm-related damage. For challenging or unsafe conditions, homeowners can rely on professional inspectors from Covenant Roofing, who are trained to safely evaluate damage to roofs, siding, windows, and other structural components.

Initial Assessment: What to Inspect

After ensuring safety, it’s time to assess your property systematically. Start from the exterior: examine the roof, shingles, gutters, siding, and fascia for wind, hail, or water damage. Look for missing shingles, dents in gutters, detached downspouts, broken siding, and any fallen trees or branches that may have impacted the structure. Capture wide-angle and close-up photos to document each area, making note of any visible damage.

Next, inspect the interior of your home for water intrusion or structural damage. Check ceilings, walls, floors, and attics for water stains, sagging materials, or mold growth. Take note of personal property affected by the storm, including furniture, electronics, appliances, carpeting, window treatments, clothing, and artwork. Create an initial inventory of damaged items, noting approximate value and condition.

For all inspections, maintain timestamped photos and videos. Document both minor and major damage, as insurance companies require evidence for every claim component. While homeowners can begin this assessment, local experts can help ensure no detail is overlooked, particularly for hard-to-reach areas like roofs, vents, and attics. Their professional documentation often strengthens insurance claims and helps speed up the approval process.

Step-by-Step Documentation

After your initial assessment, the next step is to document storm damage in a detailed and organized manner. Proper documentation ensures your insurance claim is accurate, complete, and more likely to be approved. It also protects you from potential disputes about pre-existing damage.

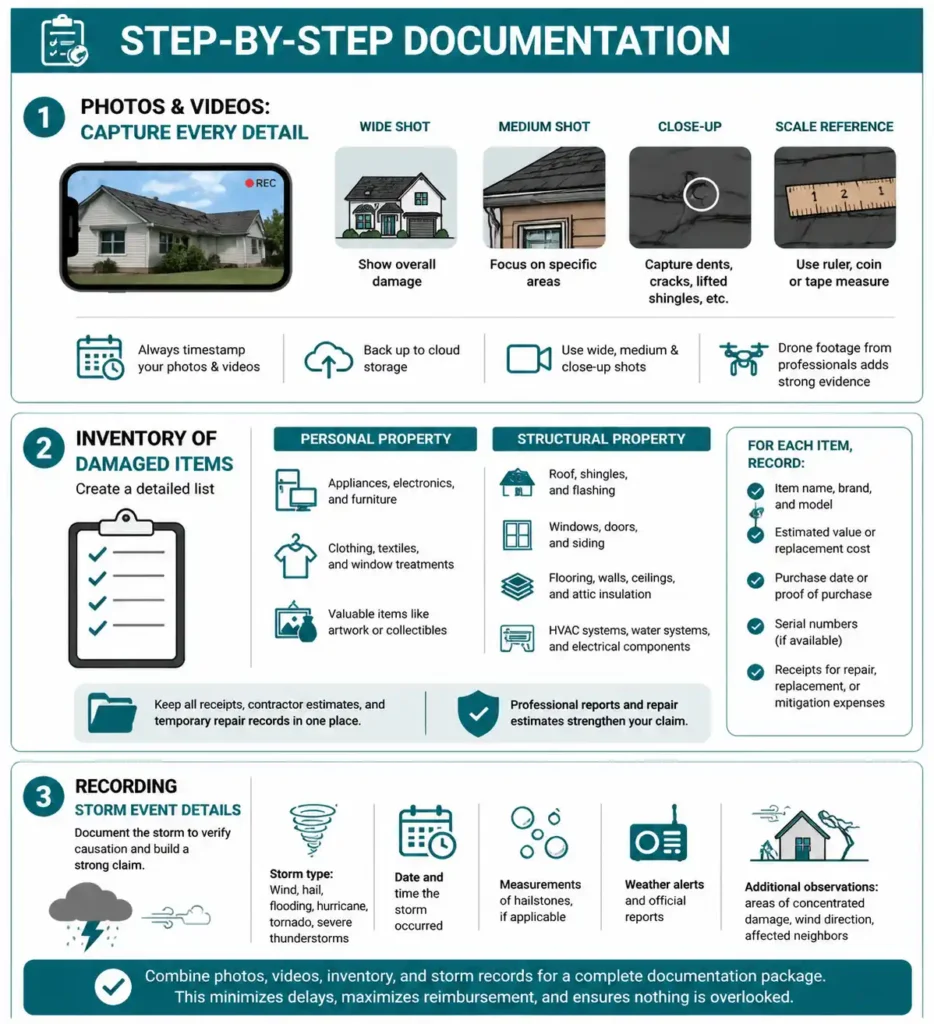

Photos and Videos: Capture Every Detail

High-quality photos and videos are the backbone of storm damage documentation. Use your phone or camera to capture:

- Wide-angle shots to show overall damage to your property, including the roof, siding, and surrounding yard.

- Medium shots focusing on specific areas such as gutters, vents, and windows.

- Close-ups of dents, cracks, lifted shingles, or broken items.

- Scale references like a ruler, coin, or tape measure to show the size of hail impact or water damage.

Always timestamp your images and videos to verify when the damage occurred. If possible, use cloud storage to back up all media for easy sharing with your insurance adjuster. Wide, medium, and close-up shots together provide a complete visual record, making it easier for insurers to assess the damage without overlooking any detail.

Professional inspectors, such as Covenant Roofing, can supplement homeowner documentation with high-resolution drone footage of roofs, vents, and hard-to-reach areas. This additional evidence can be crucial for documenting roof damage types like hail dents, missing shingles, or wind-lifted flashing.

Inventory of Damaged Items: Create a Detailed List

A thorough inventory of damaged property helps quantify losses and supports reimbursement claims. Include both personal property and structural property:

Personal Property:

- Appliances, electronics, and furniture

- Clothing, textiles, and window treatments

- Valuable items like artwork or collectibles

Structural Property:

- Roof, shingles, and flashing

- Windows, doors, and siding

- Flooring, walls, ceilings, and attic insulation

- HVAC systems, water systems, and electrical components

For each item, record:

- Item name, brand, and model

- Estimated value or replacement cost

- Purchase date or proof of purchase

- Serial numbers if available

- Receipts for repair, replacement, or mitigation expenses

Organizing this inventory allows your insurance adjuster to review losses efficiently. Keep all receipts, documentation of temporary repairs, and contractor estimates in one place. Homeowners in Greeneville, TN, can rely on Covenant Roofing to provide professional reports and repair estimates for both roof damage and personal property, improving the accuracy and success of insurance claims.

Recording Storm Event Details

Documenting the storm event itself provides context and verifies causation. Include the following:

- Storm type: wind, hail, flooding, hurricane, tornado, or severe thunderstorms

- Date and time the storm occurred

- Measurements of hailstones, if applicable

- Weather alerts and official reports from local stations

- Additional observations: areas of concentrated damage, direction of wind impact, or affected neighboring properties

Recording these details establishes a clear timeline for your insurance adjuster and helps prevent disputes about when the damage occurred. It also strengthens your claim in cases of property damage insurance disputes or when filing for recoverable depreciation. By combining photos, videos, itemized inventory, and storm event records, homeowners create a comprehensive package ready for submission. This structured approach minimizes claim delays, maximizes reimbursement, and ensures all affected areas, including roof, siding, windows, and personal property, are accounted for.

Organizing Documentation for Your Insurance Claim

Once you have collected photos, videos, and inventory lists, it’s essential to organize them effectively. A structured filing system ensures that your insurance adjuster can review your claim quickly and accurately.

Tips for organizing documentation:

- Create separate folders for Exterior Damage, Interior Damage, Personal Property, Receipts, and Contractor Reports.

- Backup all files in cloud storage for easy access and sharing.

- Maintain communication logs: emails, texts, and phone calls with insurers, contractors, or adjusters.

- Include repair estimates, emergency mitigation receipts, and daily diaries documenting ongoing damage or observations.

Working with Professionals

In many cases, a professional evaluation is necessary to document storm damage thoroughly.

Roofing or Property Inspection

Professional contractors can inspect roof damage types (shingles, flashing, gutters, vents), structural elements, and personal property. Their reports include high-resolution photos, measurements, and repair recommendations, all of which support insurance submissions.

Public Adjusters or Legal Support

If claims are complex or disputed, a public adjuster or legal professional may be needed. They ensure that your documentation meets insurer requirements and can advise on insurance bad-faith cases or fair settlement negotiations. Having expert support reduces mistakes, speeds up claims, and ensures all property and damage types, including roof, siding, windows, doors, floors, walls, ceilings, and personal belongings, are properly documented.

Filing Your Insurance Claim

When your documentation is complete, filing the claim should follow a clear process:

- Contact your insurance company promptly with your policy number and claim type.

- Submit organized photos, videos, inventory lists, receipts, and contractor reports.

- Clearly describe the storm event, including date, time, type, and observed damage.

- Track the claim number, adjuster contact, and filing timeline.

- Keep copies of all submissions for your records.

By providing complete and organized documentation, homeowners improve their chances of full reimbursement for both structural property and personal items affected by storm, wind, hail, or flooding.

Adjuster Interaction and Follow-Up

During an adjuster visit, ensure all damage is accessible and clearly documented:

- Guide them through the roof, siding, windows, and interior areas.

- Provide your inventory and receipts for damaged property.

- Record adjuster names, dates, and key findings.

- Note any additional damage discovered after submission and update your documentation.

Professional inspections from Covenant Roofing can accompany adjuster visits, verifying damage and helping homeowners in Greeneville, TN, present a comprehensive, credible claim.

Common Mistakes to Avoid

- Repairing or cleaning damage before documenting: this can reduce claim validity.

- Incomplete or missing photos/videos: wide, medium, and close-up shots are essential.

- Failing to track receipts or proofs of purchase: without these, insurers may undervalue your claim.

- Ignoring secondary damage: water intrusion or mold that develops later can affect settlement.

- Not reporting living expenses: if you must temporarily relocate, track all related costs for reimbursement.

Avoiding these errors ensures smoother, faster claims and reduces the likelihood of disputes.

Next Steps for Greeneville Homeowners

- Begin documentation immediately after the storm while ensuring safety.

- Organize all evidence, including photos, videos, inventory lists, receipts, and storm details.

- Schedule a professional inspection with Covenant Roofing to verify damage, prepare repair estimates, and support your claim.

- Submit a complete and structured claim to your insurance company.

- Track adjuster visits, follow up promptly, and maintain logs of all communication.

- Evaluate repair or replacement options with expert guidance to prevent further deterioration of the property.

Following this approach protects your home, maximizes insurance reimbursement, and ensures you have a clear record of all damages, from roof and structural elements to personal property and appliances.